Six Percent. That Is How Many Advertisers Trust the Numbers That Retail Media Sends Them.

The $71 billion retail media industry promised to close advertising's oldest open question. The data shows it hasn't. Here is why — and what it is going to cost.

In 1876, John Wanamaker, who had built one of America’s first department stores in Philadelphia, made the observation that would follow the advertising industry for the next 150 years: half of his advertising spend was wasted, and he could not figure out which half. The line became the most quoted complaint in the history of marketing not because it was clever but because it remained accurate for so long. You placed an ad in a newspaper and you hoped. You bought a television commercial and trusted a panel of 5,000 households to represent 330 million viewers. You ran a billboard and assumed that location, repeated exposure, and human memory were doing something useful. The whole expensive enterprise rested on inference.

Digital advertising was supposed to end all of that. The internet created, for the first time, a mechanism that could theoretically follow a consumer from the moment they encountered an advertisement to the moment of purchase, producing the causal proof that print and television could never provide. The industry built impressions and click-through rates and last-click attribution models, and spent a decade discovering that what it had built was good at measuring what happened after an ad and poor at measuring whether the ad had actually caused anything. A consumer who sees a sponsored link for shoes they already planned to buy and then buys them is not evidence that the ad sold the shoes. But the model said it was, and the budgets grew accordingly.

Retail media was the industry’s most compelling answer to this problem, and the argument for it deserves to be stated in its strongest form before being examined. A retailer occupies a position that no other advertising medium has ever occupied: it owns the transaction. When a shopper buys a product at Kroger, Kroger knows the shopper’s identity, purchase history, basket composition, frequency, price sensitivity, and the precise moment of conversion. That is not an inference about consumer intent. That is a receipt. If you can connect the ad to the receipt, you have finally given John Wanamaker his answer. The loop, the industry announced, was closed.

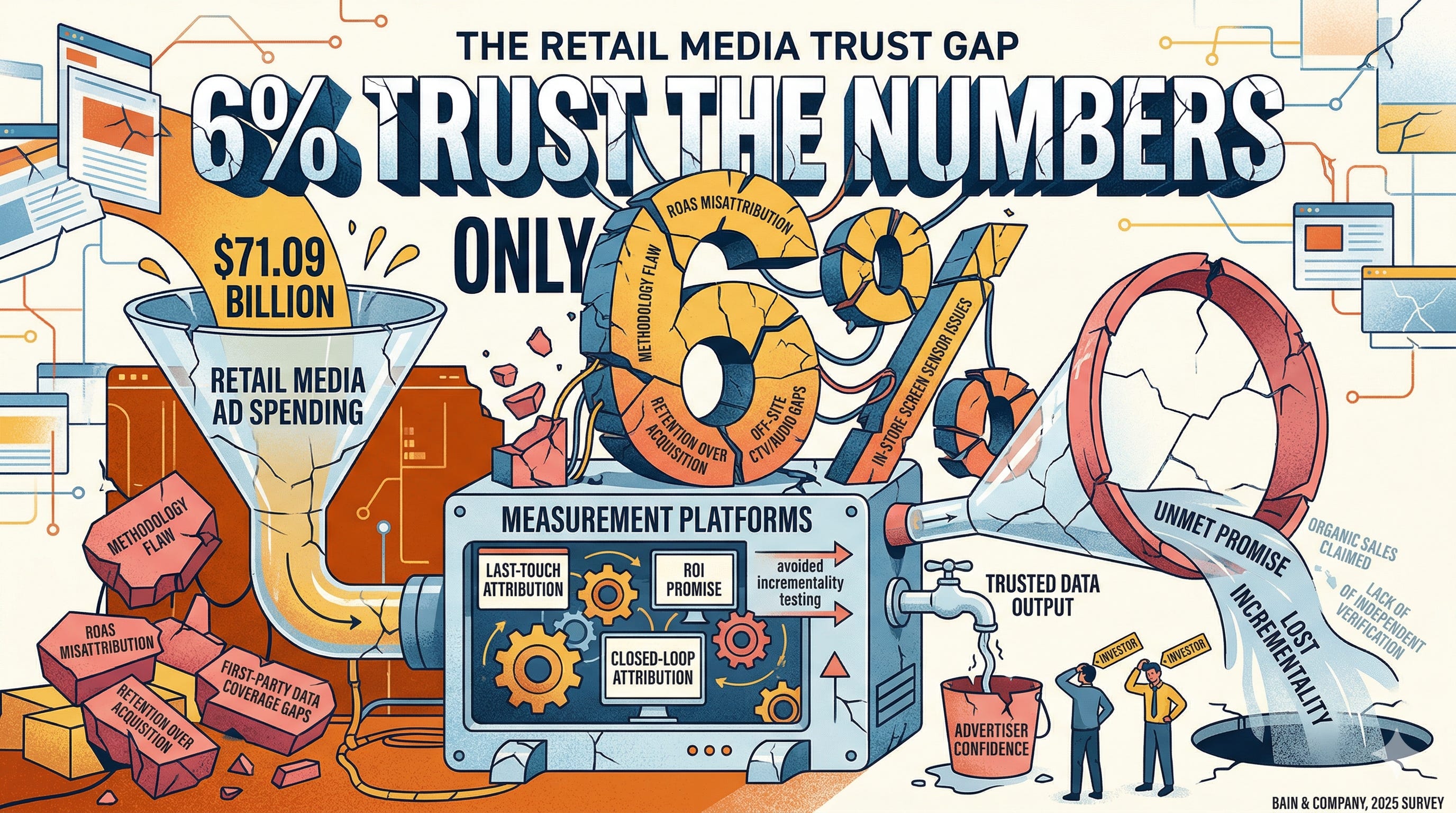

US advertisers spent $60.32 billion on retail media in 2025, according to EMARKETER’s December 2025 forecast, and will spend $71.09 billion in 2026, the fastest-growing major advertising channel in the world, expanding at roughly 18 percent annually against a broader market growing at 4.3 percent. The promise is on every slide deck and in every conference keynote: first-party data, purchase-intent audiences, closed-loop attribution, proof of ROI. The channel has attracted more than 200 retail media networks globally, with over 80 operating in the United States alone, ranging from Amazon Ads and Walmart Connect at the top to grocery chains including Albertsons Media Collective, Kroger Precision Marketing, and CVS Media Exchange; specialty retailers like Home Depot’s Orange Apron Media, Best Buy Ads, Lowe’s One Roof Media Network, and Sephora Media Collective; and smaller but notable networks including Sam’s Club’s Member Access Platform, Walgreens Advertising Group, Macy’s Media Network, Kohl’s Media Network, 7-Eleven’s Gulp Media, Ace Hardware’s RedVest Media launched in 2025, and Petco’s emerging network. Every retailer with a loyalty programme and a website is building one, and the commercial logic is obvious: advertising generates 50 to 70 percent operating margins against the 3 percent that the underlying retail business produces.

This Tuesday, April 14, the Interactive Advertising Bureau (IAB) convenes its Connected Commerce Summit in New York, the industry’s most focused annual gathering on the specific business of retail media; and the session titles that appear on the agenda are more honest than anything that tends to appear in a keynote at a retail media launch event. Executives from Colgate-Palmolive, Mondelēz, Bayer, Monster Energy, and Mars Wrigley will appear alongside platform leaders from Target Roundel, Best Buy Ads, Grocery TV, Dollar General, 7-Eleven, and Ace Hardware’s newly launched RedVest Media network to discuss sessions titled, with a directness that the industry has usually reserved for private conversations: ‘Making Omnichannel Measurement Real’, ‘Building the Transparent Commerce Media Tech Stack’, and ‘Connecting Off-Site Media Signals to Sales Outcomes’. The final panel of the day is titled ‘The Great Debate: Will Retail Media Be the Casualty of AI-Driven Commerce?’ — a question that, as this article will attempt to demonstrate, would have been considered professionally hazardous to ask in public as recently as two years ago. The right questions are finally being asked. The fact that they are being asked at the IAB’s industry summit rather than answered by the retailers selling the product is the point.

Bain and Company surveyed advertisers to determine how many trust the measurement numbers they receive from retail media networks. The answer is 6 percent. Not 60. Not 16. Six. The industry running on the most data-rich advertising proposition in the history of the medium is being trusted, by the people spending the money, at about the rate you would trust a stranger you met ten minutes ago. Wanamaker’s problem has not been solved. It has been monetised at scale.

“Only 6% of advertisers fully trust retailers’ reported media metrics.” — Bain and Company, 2025

· · ·

The measurement crisis begins with a methodology called last-touch attribution, and understanding it is the key to understanding everything that follows. An analysis of the top sixteen ad types across the six largest retail media networks in the US (Amazon Ads, Target Roundel, Walmart Connect, Kroger Precision Marketing, Criteo’s commerce media platform, and Instacart Ads) found that 80 percent of them assign 100 percent of the credit for a purchase to the final advertisement the buyer encountered before completing the transaction. Every other touchpoint in that buyer’s journey, the television commercial they saw six months ago that introduced the brand, the social media post that kept the brand salient, the display ad that appeared when they were considering switching to a competitor, is credited with zero.

The critical flaw in this methodology is not that it measures the wrong ad. It is that it frequently credits the ad for a sale that was already happening. Consider a consumer who has bought the same protein bars every three weeks for two years. On Thursday, Kroger Precision Marketing serves them a sponsored product for those bars. On Saturday, they buy the bars, as they were always going to. KPM’s attribution model records a successful campaign. The actual question, did the ad change this consumer’s behaviour in any way, was never asked, because answering it would require comparing the consumer’s behaviour against a control group that never saw the ad. That methodology has a name: incrementality. And it is precisely what the industry has been avoiding.

This avoidance is not accidental. Incrementality testing produces lower ROAS numbers than last-touch attribution, because it strips away the organic demand that the last-touch model was claiming as advertising success. If a brand’s loyal customers would have repurchased without any advertising at all, which many of them would, then the ROAS attributable to genuinely incremental sales is substantially lower than what the platform dashboard shows. Skai and Stratably surveyed 166 retail media advertisers for their 2026 State of Retail Media report and found that while 71 percent of brands now consider incrementality their most important KPI, only 20 percent are good at both measuring it and acting on the results. The remaining 80 percent are making budget decisions against numbers they cannot independently verify and privately do not trust.

The distinction between retention and acquisition campaigns makes this problem even starker, and it is a distinction that retail media’s standard measurement frameworks have almost entirely ignored. Retention campaigns reaching existing loyal buyers to maintain their purchase frequency look outstanding on a ROAS metric because the buyer was going to purchase anyway, and the ad gets full credit. Acquisition campaigns reaching consumers who have never bought the brand, or who are actively considering switching from a competitor require proving genuinely incremental demand, because there is no baseline purchase pattern to misattribute. They look worse on ROAS not because they are worse advertising but because they are doing harder work. The 2025 ANA study on retail media found that 62 percent of retail media budgets go to audiences who are already brand buyers. The brands spending $71 billion on retail media are using more than half of it to advertise to people who were already their customers, measuring the effectiveness of that spend with a methodology that guarantees a favourable result, and calling the combination a closed loop.

PepsiCo’s test with Skai capabilities across Amazon DSP, where the company specifically optimised for new-to-brand customers rather than existing buyers and measured results using incremental ROAS, unlocked over 80 percent new-to-brand ROAS, a metric that looks different from, and less flattering than, overall ROAS precisely because it is honest. That test is instructive not because PepsiCo discovered some breakthrough but because it demonstrated how different the numbers look when the measurement methodology is designed to find the truth rather than confirm the budget allocation. Jason Wescott of WPP Media has said the overreliance on ROAS as the benchmark of value is over, and independent, transparent measurement is the baseline. CJ Pendleton, Chief Strategy Officer at Matrixx CPG, has named the commercial consequence without diplomatic softening: the platforms that solve for incrementality will earn the lion’s share of CPG investment while those that don’t will likely die on the vine.

· · ·

Understanding why the measurement crisis persists requires understanding what retail media’s first-party data actually is, and what it is not, across the spectrum of networks that are selling it. At the top of the market, the data proposition is real. Amazon’s $68.63 billion in global advertising revenue in 2025, confirmed by the company’s Q4 earnings release, with $21.32 billion in that quarter alone is built on direct transaction data from hundreds of millions of consumers who have bought on Amazon’s platform. Amazon knows your purchase frequency, your basket composition, your price sensitivity, your device preferences, and the moment your repurchase window opens. Walmart, which generated $6.4 billion in global advertising revenue in 2025, up 46 percent year-over-year per its February 2026 earnings, is building toward comparable depth: CFO John David Rainey noted that advertising and membership together accounted for a full third of Q4 2025 operating income, describing a business where advertising has become structurally important to profitability rather than incidental to it.

But Amazon and Walmart together hold approximately 87.7 percent of US digital retail media advertising spend. Amazon at roughly 79.7 percent and Walmart at about 8 percent, per EMARKETER’s December 2025 platform analysis. EMARKETER further projects that approximately 89 percent of the $10.77 billion in incremental retail media growth in 2026 will go to those same two companies. That leaves the other 80-plus US retail media networks competing for a slice of the market that, in incremental terms, is barely growing for anyone else. They are competing for smaller budgets with weaker data infrastructure, using the same first-party data marketing language as Amazon, and delivering a product that Georgia-Pacific, the consumer goods company, described in terms that should give every CPG brand media buyer pause.

Georgia-Pacific evaluated approximately 40 retail media networks over several years as it shifted more than 20 percent of its total media budget to the channel. Its Digital Marketing Director’s conclusion, reported in 2024, was precise and devastating: they told you they had first-party data, but they were not always giving first-party data to activate against them. The company was not describing an experience with a single bad actor. It was describing a pattern across a systematic evaluation of 25 networks it trialled. The data being sold as first-party was, in a material number of cases, something else: modelled segments, third-party augmentation, or loyalty data with coverage gaps so significant that the targeting precision implied in the pitch bore little relation to what was actually available.

EMARKETER identified the structural reason in February 2026: even genuinely robust first-party datasets reflect only shoppers who have engaged with the retailer’s loyalty or login system. That excludes irregular buyers, lapsed customers who still influence category dynamics, high-value prospects who are in-market but have never used that retailer’s card, and entirely new-to-category consumers who represent the actual growth opportunity for most CPG brands. A brand trying to find new customers which is the primary purpose of brand marketing investment is using targeting data that systematically excludes the people it most needs to find. The closed loop that retail media promises is real for the customers who are already inside it. For everyone outside it, retail media is programmatic display with better demographic labels.

The way retailers build audience segments compounds this problem in ways that rarely surface in a sales meeting. The standard taxonomy available across most retail media networks (heavy category buyers, lapsed purchasers, competitive brand switchers) consists of demographic buckets with transaction labels attached, and those constructs were designed for programmatic display targeting in 2010. A retailer with years of weekly purchase history across tens of millions of loyalty members has, in principle, the raw material to build something genuinely different: individual-level purchase cycle models that predict when a specific household is entering its consideration window, price elasticity signals that identify the moment a loyal customer is vulnerable to a competitor’s promotion, declining frequency patterns that flag at-risk customers before they switch. The most sophisticated networks like Kroger Precision Marketing through its 84.51 analytics arm, which works with purchase data from over 60 million loyalty households, are beginning to build in this direction. Most networks are selling the same five segments to every brand that will buy them.

· · ·

The audience segmentation problem becomes more severe, not less, when retail data is used to target audiences outside the retailer’s own properties. Off-site retail media, the practice of using a retailer’s first-party data to serve ads on external publisher websites, connected television, programmatic display, and audio is the fastest-growing component of the channel. In Q4 2025, 60 percent of Walmart Connect’s self-serve display spend went to offsite inventory, per Tinuiti’s Digital Ads Benchmark Report. Target’s Roundel reports that more than 30 percent of partner media spend now happens off its owned platforms. The retailers’ audiences are being used to buy ads everywhere. The question of whether the measurement travels with them has a troubling answer.

CTV is where the audience segmentation problem is most visible, and most consequential. Retail media’s extension into connected television is one of the industry’s most celebrated developments: Amazon’s Prime Video ad inventory, which delivered ads to an average of 315 million viewers globally in Q4 2025; Walmart Connect’s CTV capability through the $2.3 billion Vizio acquisition; Kroger Precision Marketing’s partnership with Magnite to extend into CTV. The proposition is genuinely compelling. Use purchase-based audience data to reach household-level audiences in the most engaging media environment available. The measurement reality is described, with characteristic bluntness, by Advertising Week’s 2026 analysis of CTV performance: measurement is still stuck two or three years behind the channel’s growth, and most CTV campaign reporting is comparing apples and oranges.

Comscore’s 2026 State of Programmatic Report, based on more than 200 media buyer respondents, found that 87 percent say cross-channel performance metrics inside programmatic platforms are critical or valuable for decision-making, and simultaneously that CTV measurement challenges like inconsistent reporting windows, limited cross-device visibility, and fragmented clean room integrations, remain significant barriers. The problem is not that CTV is unmeasurable. It is that the audience segment that entered the CTV buy as a retail-data-defined group of heavy category buyers cannot be tracked through the living room, through the consideration period, and back to a verified purchase at a retail location, without a data infrastructure connecting all three environments that most networks have not yet built. Kroger’s partnership with Magnite is a step toward it. The measurement framework that closes that loop does not yet exist at scale.

Audio faces the same fundamental challenge, with an additional layer: the format is inherently harder to connect to a purchase outcome because a consumer listening to a podcast while cooking dinner is not in a purchase moment the way a consumer on a search results page is. Programmatic audio is growing as Comscore’s 2026 report projects audio will capture 10 percent of programmatic budgets on average, with 21 percent of marketers reallocating from linear radio. Comscore itself launched audio targeting and measurement capabilities with The Trade Desk in January 2026, providing contextual targeting across 4.6 million podcasts and campaign measurement without relying on identity signals. The measurement progress is real. The gap between a retail-defined audience segment applied to a streaming audio buy and a verified purchase outcome at a physical or digital retail location remains wide enough that most brands treating audio as a performance channel are doing so on attribution windows that cannot distinguish advertising causation from coincidence.

Programmatic display, the channel that retail media was supposed to supersede with its superior first-party data, has quietly absorbed the segmentation problem rather than solved it. When a retailer’s audience segments are activated through The Trade Desk, DV360, or any other major DSP and served as display impressions across the open web, the impression appears on a publisher’s page, the cookie or identifier connects to the retail audience profile, and the attribution model waits for a subsequent purchase on the retailer’s platform. If the purchase occurs on a different retailer like the consumer saw Kroger’s display ad, considered the product, and bought it on Amazon because the price was lower, Kroger’s model counts a miss while the sale happened regardless. If the consumer was already planning to buy, Kroger’s model potentially counts a hit for a behaviour the ad did not influence. The closed loop that retail media promised was closed at the transaction point. It remains open everywhere the ad ran before the transaction.

Topsort, the commerce media platform that partnered with Skai in September 2025 to enable unified access to retail media networks across 40 countries through a single API integration, is building toward the cross-channel measurement consolidation that these problems require. Its architecture treats the retailer audience as a portable targeting signal rather than a siloed network property, which is the structural shift that cross-channel retail media measurement needs. Pentaleap, which in July 2025 launched real-time bidding for sponsored product ads through its Teads partnership enabling, for the first time, fully programmatic sponsored products on retailer sites is creating the supply-side transparency that makes cross-channel attribution auditable. These are meaningful technical contributions. They are building components of the infrastructure that the measurement problem requires. The full infrastructure does not yet exist anywhere except at Amazon, and only partially at Walmart.

· · ·

The most interesting and least honestly discussed extension of retail media is the physical store, and the timing of its emergence as an industry priority reveals something important about the online channel’s maturity. When onsite inventory runs out, when every available sponsored product slot on a search results page is sold and the user experience of adding more would drive shoppers away, the channel’s next move is either offline or inside someone else’s inventory. Both have happened simultaneously. The offsite expansion into CTV and programmatic display has been widely discussed. The in-store screen expansion has received less scrutiny, which is unfortunate, because it is where the measurement crisis is most acute and where the parallel with a $200 million failure in a Dallas warehouse is most directly relevant.

Retail stores were advertising’s original closed-loop environment. The shopper arrives with a purchase intent, encounters a display, makes a decision, and the transaction happens within the same four walls. Brand managers have understood this since the 1950s, and the physical store, the endcap, the in-aisle display, the checkout lane has always been the most valuable last-mile advertising surface available to CPG brands. What retail media has now added is the possibility of making that surface programmatic: digital screens in the aisle that can be targeted, measured, and optimised in near-real time, connected to the same loyalty data infrastructure that powers online retail media. This is the promise of Digital Out-of-Home within the retail environment, a $7.4 billion market in North America in 2026, according to Fortune Business Insights, and it represents a genuine opportunity that traditional DOOH advertising has historically left uncaptured because it was not connected to transaction data.

Kroger committed in June 2025 to a nationwide expansion of in-store digital screens through its partnership with Barrows Connected Stores, with Christine Foster, SVP of Kroger Precision Marketing, noting that the grocer sees the physical store as one of the most underutilised platforms for brand storytelling. Albertsons launched a digital display network in 80 stores in July 2025 through Stratacache. Hy-Vee deployed more than 10,000 screens across 400-plus locations with Grocery TV. Best Buy announced full-store takeover packages. Even Save-a-Lot is plotting an in-store rollout across 900 locations. Paul Brenner, SVP of retail media at In-Store Marketplace, reported in January 2026 that his firm had 20 active RFPs from retailers for 2026 screen deployments, some requesting thousands of units per retailer. The investment thesis is clear: over 91 percent of food and beverage purchases still happen in physical stores, yet 99 percent of retail media advertising has been online. The physical store is the single largest measurement gap in the entire retail media landscape.

The DOOH connection matters here because it is the technical framework that makes in-store screens programmable and measurable at scale. A screen in the frozen food aisle, running on DOOH infrastructure, can in principle be served to a shopper whose loyalty profile indicates they have not purchased a particular brand for six weeks — a lapsed buyer, targeted at the precise moment they are standing in front of the product. That is a targeting capability that outdoor DOOH on a highway billboard can never match, and it is the reason that the smart money in advertising infrastructure is watching in-store retail media very carefully. When a screen at the Kroger dairy case can trigger a sponsored display based on the household loyalty profile of the shopper scanning their app at the same time, and when the subsequent basket scan closes the attribution loop at the same transaction, the closed-loop measurement that online retail media has been claiming becomes something it actually can deliver.

The reason it has not delivered this yet is the Cooler Screens lesson, made permanent in a Dallas warehouse. Cooler Screens installed 10,300 smart refrigerator door screens across 700 Walgreens locations, claiming 100 million monthly impressions from sensors that turned out to be counting bathroom trips, shopping carts, and shadows. The screens generated $215 per door annually against a contractual minimum of roughly double that. When CEO Arsen Avakian cut data feeds to 100 stores during the December 2023 holiday season in a contract dispute, screens went white across refrigerator aisles at the industry’s most commercially sensitive moment. The $200 million lawsuit followed. The hardware, nearly $50 million worth, is sitting in Texas. The measurement system had been counting the wrong things, calling them impressions, and reporting the result as evidence of a closed loop. In-store retail media, run correctly, could finally deliver what the DOOH industry has always promised and what grocery advertising has always needed. Run without genuine measurement infrastructure, it produces lawsuits and warehouses.

Christine Foster’s comment about not wanting the screens to feel like Times Square is the tension that the industry has not resolved. A screen designed to be invisible is not a high-attention advertising placement. A screen designed to attract attention is a disruption to the shopping experience the retailer depends on. These two goals are not reconcilable without measurement that tells you which placement intensity produces the best combination of advertising effectiveness and shopper retention which is precisely the measurement that the IAB’s December 2025 in-store standards framework, which defines store zones and impression metrics but does not address individual-level attribution through loyalty data or cross-channel purchase journeys, does not yet require.

· · ·

Criteo, the independent commerce media company that is probably the industry’s most instructive case study, is not a retailer. It is a technology platform operating both as a demand-side platform helping brands buy across retail media inventory and as a supply-side platform helping retailers monetise their audiences and it built the technical infrastructure on which a significant share of the industry runs. Criteo is not Amazon or Walmart. It is the middleware. That distinction matters enormously for understanding its measurement position, because Criteo sits in the measurement gap itself: it processes transactions between retailers and brands, which means it sees both the ad delivery and the attributed purchase signal, but it does not own either the retailer’s closed-loop data or the brand’s independent measurement. In September 2025, Criteo became Google’s first onsite retail media partner through Search Ads 360. The announcement positioned this as a significant expansion. It also reveals that an independent infrastructure company, after building integrations with more than 200 retailers globally and completing a $380 million acquisition of IPONWEB in 2022, needed Google’s advertiser demand to make its retail media infrastructure commercially viable. That is not a failure. It is a structural reality about where the leverage in retail media actually sits.

The agencies that manage the advertising investment of the brands spending these billions are navigating the same structural terrain, with varying degrees of conflict. Publicis Groupe, which reported 5.9 percent organic growth in Q2 2025 and maintained its position as the industry’s growth leader, owns both CitrusAd, a retail media technology platform powering multiple retailer networks and Epsilon’s data infrastructure, which powers audience segmentation for clients including Kroger. Publicis is the agency advising brands on which retail media networks to trust, while simultaneously operating the technology those networks run on and the data infrastructure those networks use. CEO Arthur Sadoun’s framing of the company’s 2026 strategy as building agentic solutions that deliver business outcomes at a moment when 95 percent of AI projects fail is directionally accurate. The structural position his company occupies in the retail media ecosystem is worth noting alongside it. WPP’s $60 billion annual media investment operation, operating under the WPP Media brand after retiring GroupM in 2025, is in a different position: managing at massive scale without the same proprietary data infrastructure, which creates both a cleaner measurement posture and a more exposed commercial position in a world where data ownership is becoming the primary competitive variable.

The $60 million FTC settlement that Instacart reached in December 2025 is, on the surface, a consumer protection story: the commission alleged that the company’s advertising and billing practices misled consumers with promises of free delivery that masked mandatory fees adding up to roughly 15 percent of order value. But it connects to the retail media measurement story in a specific way. Instacart is one of the larger retail media networks outside the Amazon-Walmart duopoly, generating close to $1 billion in annual US advertising revenue according to EMARKETER projections. Its advertising proposition to CPG brands rests on the same closed-loop claim as every other network: reach high-intent grocery shoppers at the moment of purchase, measure results through Instacart’s transaction data. The FTC’s finding that Instacart’s representations to consumers were not accurate about its own fees, the basic facts of how much the platform costs, raises a question about whose methodology is being used to measure everything else the platform claims about the effectiveness of the advertising it sells. A platform that was found to have misrepresented its cost structure to consumers was simultaneously providing CPG brands with closed-loop performance data about the advertising those same consumers were shown. The FTC settlement is about consumer protection. The measurement implication is about advertiser protection.

The Instacart case is the Cooler Screens pattern at a different level of the ecosystem. Both companies built their retail media products on a specific measurement claim. Cooler Screens on impression counting that was measuring bathroom trips; Instacart on a consumer transparency standard that the FTC determined was not being met. And both cases ultimately revealed that the numbers being used to justify advertising investment were produced by parties with competing interests in what those numbers showed. This is the structural condition that produces the 6 percent trust figure. It is not that retailers and platforms are deliberately falsifying data. It is that the entity producing the measurement has a financial interest in the measurement being favourable, and the entity receiving the measurement has no independent mechanism to verify it.

This is precisely where demand-side and supply-side platforms, the DSPs and SSPs that sit between advertisers and retail media networks, have an underutilized and under-appreciated role to play. Because independent DSPs are not retailers and do not own the inventory they are buying, they occupy a structurally different measurement position than the retail networks themselves. When The Trade Desk runs a campaign across Walmart Connect, Kroger Precision Marketing, and Instacart simultaneously, it has cross-network impression data that none of those three networks can see independently, data that, in principle, allows a brand to detect frequency overlap, audience duplication, and attribution double-counting that individual network dashboards systematically obscure. The problem is that The Trade Desk’s Retail Index marketed as a neutral benchmark for cross-network performance is produced by the same DSP routing spend through those networks, with financial agreements in place with the data providers whose segments are being scored. Grading your own homework is a problem at the retailer level. Outsourcing the grading to your DSP, whose revenue depends on routing your spend efficiently, does not fully solve it. Andrew Casale of Index Exchange has said publicly that some supply-side vendors extract more value than they create is a notable observation from the CEO of an SSP, and one that applies with equal force to some DSPs. What the independent DSP ecosystem could provide, if it chose to build the capability, is cross-network attribution that no single retail media network can produce: a unified view of where an advertiser’s spend went, what audiences it actually reached in deduplicated terms, and which network attributed the same consumer’s purchase as its own success. Rajeev Goel of PubMatic, whose AgenticOS platform is building toward agent-driven media buying, has described the value chain compression that agentic AI enables as an opportunity to create more transparent, direct connections between buyer and seller. The measurement opportunity in that compression is real. The DSPs and SSPs that build toward it, rather than routing around the transparency question, will earn a position in the measurement ecosystem that the retailers and their networks cannot credibly occupy.

· · ·

Adobe Analytics reported that AI-driven traffic to US retail sites increased 805 percent year-over-year on Black Friday 2025 and 670 percent on Cyber Monday. ChatGPT now drives more than 20 percent of referral traffic to Walmart.com, approximately 15 percent to Target, and 10 percent to eBay, per a December 2025 MetaRouter analysis. Salesforce reports that 39 percent of consumers, and more than half of Gen Z, already use AI for product discovery. These numbers are still small in absolute terms relative to human-browsed retail traffic. They are not small in directional terms.

The sponsored product being the foundational revenue unit of retail media, projected to account for $38 billion in advertiser spend in 2025 is a format built for human browsing. A consumer loads a search results page, sees a placement, processes the creative, and decides. An AI agent managing a household’s weekly grocery order does not load a search results page. It queries the inventory API, checks price and availability, cross-references reviews and nutritional data against stated preferences, and completes the transaction without ever rendering a sponsored product or registering an impression in any attribution model. The ad never ran. The attribution window opened and closed around a transaction it could not see.

This is where Generative Engine Optimisation connects directly to the measurement problem, and the connection is not a trend analogy. It is a causal relationship. GEO as the practice of ensuring that product data is complete, structured, and machine-readable so that AI agents can confidently discover and recommend it addresses exactly the data quality gap that has made retail media measurement unreliable from the beginning. The reason last-touch attribution dominates retail media is partly technical inertia, but it is also a symptom of insufficient data discipline: if the signal connecting an ad impression to a purchase outcome were as clean and structured as a product API response, incrementality testing would be computationally trivial. GEO forces brands to build the data infrastructure that makes products findable by agents. That same infrastructure, applied to the advertising side, makes ad exposures linkable to purchase outcomes with the kind of precision that closed-loop measurement has promised and not delivered. The brands building GEO discipline are, almost without realising it, building the foundation for measurement that actually works.

Walmart’s Sparky, the agentic shopping assistant that reached half of all Walmart app users and generated 35 percent higher average order values than standard search, has already begun testing sponsored prompts inside its conversational interface that an advertiser can pay to be the recommendation Sparky surfaces when a consumer asks for a product category. Walmart CEO Dave Guggina said on the Q4 2025 earnings call that the company is learning as it goes on how advertising works in agentic commerce. That honesty is more valuable than any measurement dashboard Walmart could have published instead. Amazon’s Rufus assistant, with 300 million users and $12 billion in attributed sales in 2025, is facing the same question. The retailer that invented retail media and the retailer that followed it most closely are both trying to figure out what an ad looks like when the shopper cannot see it.

· · ·

The measurement problem is solvable. This is the critical point, because the failure to solve it is commercial rather than technical, and commercial barriers move when the financial incentives change. The infrastructure that would genuinely close the loop has been described accurately by the industry’s own standards bodies, the IAB and MRC published retail media measurement guidelines in January 2024 but guidelines describe what should happen, not what does. What does happen is that the entity producing the measurement has a financial interest in that measurement being large, and the entity receiving the measurement has no systematic mechanism for independent verification. There is a phrase for this in education: grading your own homework. In advertising, it has been the norm for thirty years. In retail media, which was supposed to solve the problem, it has become the structural foundation.

A small ecosystem of independent measurement companies has built the tools that could break this cycle, and the most interesting thing about them is how small they remain relative to the problem they are trying to solve. Haus, founded by former Google and Facebook data scientists and backed by meaningful venture capital, runs incrementality measurement through geo-based holdout experiments: it divides a brand’s geographic markets into exposed and unexposed groups, measures the difference in sales outcomes, and produces an estimate of genuinely incremental lift that is not filtered through the retailer’s attribution model. Measured, which raised $21 million in Series B funding and works with hundreds of brands across their full media portfolio, offers multi-touch attribution combined with incrementality testing, allowing brands to evaluate not just whether retail media is working but how it compares against other channels competing for the same budget dollar. Northbeam applies machine learning to attribution modeling across channels, helping brands understand which combination of touchpoints actually contributed to a sale rather than which single touchpoint the last-touch model credited. NCSolutions, which connects advertiser campaign data to actual purchase outcomes using purchase-based measurement drawn from over 150 million US households via retail loyalty programmes, operates at the intersection of panel-based measurement and first-party retail data — providing a verification layer that does not require the retailer’s own attribution system to be trusted. Neustar, now a TransUnion company, offers campaign measurement and media mix modelling that treats retail media as one input among many rather than a closed system that defines its own success.

These companies exist. They work. The brands that use them describe, consistently, a gap between platform-reported ROAS and independently measured incrementality that is large enough to change budget allocation decisions. Ryan Verklin, Retail Media and Paid Media Senior Lead at Bayer — who will participate in the IAB Connected Commerce Summit’s ‘Great Debate’ panel next week — won AdExchanger’s Best In-House Media Operation award specifically by pioneering self-serve retail media with incremental measurement at the centre of the strategy rather than the margin. The capability exists. It is not scaling. And the reason it is not scaling is a cascade of commercial barriers that are worth naming precisely.

The first barrier is data access. An independent measurement firm running a holdout experiment needs impression-level exposure data from the retail media network, specifically, a list of which consumers were served the ad and when, linked to purchase outcomes after the campaign. Most retail media networks do not provide this data to third parties. Amazon Marketing Cloud offers impression-level data within its clean room environment, which means Haus or Measured can run holdout analysis there but only within AMC’s infrastructure, under AMC’s terms, using AMC’s identity graph. This is meaningful progress and simultaneously a measurement system that still relies, at the data layer, on the entity being measured. Kroger Precision Marketing, to its credit, has been more forthcoming with clean room access for external measurement partners than most networks its size. Most networks below the top tier provide aggregate reporting with limited granularity and no access to individual impression data that would support true holdout analysis.

The second barrier is commercial inertia. A brand that is receiving ROAS numbers of 5 or 6 from a retail media network dashboard, and has not run an independent incrementality test, has no empirical reason to doubt those numbers except for the intuition, increasingly widespread, that they seem too good to be consistently true. Running an incrementality test requires budget, time, internal analytical resources, and the willingness to accept a result that might require going back to the CFO and explaining why the advertising that was reporting excellent returns has been producing lower incremental sales than the dashboard suggested. The brands that have run these tests tend not to publicise the results, because the results frequently require awkward conversations with retail media network account teams. The brands that have not run these tests tend to remain comfortable with the dashboard numbers, because the alternative is uncomfortable. This is not irrational behaviour. It is rational behaviour in an environment where the measurement system was designed by a party with an interest in large numbers, and where the cost of discovering the truth includes the cost of revising a budget allocation that current stakeholders have committed to.

The third barrier is scale. Haus, Measured, and Northbeam are formidable technical products serving sophisticated brands. They are not The Trade Desk, which reported nearly $3 billion in annual revenue. They are not IAS or DoubleVerify, which have achieved the market position and MRC accreditation to be included in standard campaign specifications at major agencies. IAS earned its first MRC accreditation for retail media measurement specifically viewability within Amazon’s ecosystem in November 2025, nearly a decade after IAS was founded. MRC accreditation for incrementality measurement within retail media networks, which is the certification that would actually address the 6 percent trust problem, does not exist. The MRC accreditation process takes approximately two years and costs hundreds of thousands of dollars per network. An independent measurement firm that wanted to achieve MRC-accredited incrementality certification across the ten largest US retail media networks would be looking at a multi-year, multi-million-dollar credentialing exercise before any agency could include it in a standard measurement specification. The economics of that path are not attractive for a venture-backed startup competing with platforms that have unlimited marketing budgets and brand recognition built over decades. The measurement ecosystem needs these companies to be significantly larger than they are, and the path to being significantly larger runs through advertiser mandates that do not yet exist, which requires advertiser sophistication that is still being built, which requires campaign results that are still too often treated as proprietary, which means the ecosystem stays smaller than the problem requires.

Closing the loop on this cascade requires, first, genuine holdout testing: a portion of the target audience is held back from seeing the ad, and the difference in purchase rates between exposed and unexposed groups is measured. Second, attribution windows must be set empirically based on documented purchase cycles for specific product categories, not selected by the platform to maximise attributed conversions, and disclosed before the campaign runs. Third, and this is the requirement that the industry’s most powerful players have the least incentive to adopt, the measurement itself must be certified by parties with no financial relationship to the platforms being measured. Integral Ad Science’s November 2025 MRC accreditation for viewability measurement within Amazon’s ecosystem is genuine progress. It measures viewability, which is the floor of advertising standards: it tells you the ad was technically capable of being seen by a human. It does not measure incrementality, which is the ceiling: it does not tell you whether seeing the ad changed what that human did. The gap between viewability and incrementality is the gap between the measurement the industry has accredited and the measurement it actually needs.

Fourth, and most foundationally, the audience data being sold as first-party must actually be first-party. This means standardised data quality audits making the kind of systematic evaluation Georgia-Pacific conducted over years available to every brand without requiring a multi-year self-funded programme. The startups building the next generation of retail media infrastructure, Pentaleap with RTB for sponsored products, Koddi with unified commerce media, Kevel with API-first ad serving built for retail constraints rather than adapted from display advertising are creating technical conditions under which data provenance becomes auditable as a structural feature of the platform rather than a voluntary disclosure. The question is whether the incumbent networks follow. The answer will depend on whether the brands writing the cheques start requiring data quality audits the way they started requiring brand safety controls a decade ago. They started requiring brand safety controls when a YouTube adjacency scandal made not requiring them commercially embarrassing. The retail media equivalent of that moment has not yet arrived. The Instacart FTC settlement and the Cooler Screens warehouse in Texas are early drafts of it.

86 percent of commerce media decision-makers in North America and Europe identified strengthening measurement and attribution as a high or critical priority for 2026, according to the November 2025 Koddi and Forrester survey. Only 12 percent had reached an advanced state of full-funnel measurement capability. The gap between the priority and the capability is 74 percentage points. That gap is the measurement crisis expressed in the industry’s own numbers about itself, and it is the most honest data point that the $71 billion market has produced.

· · ·

Possible 2026 in Miami this month, and every industry conference before and after it, will feature a version of the retail media keynote that describes a closed-loop advertising channel with unmatched first-party data and measurable ROI. The presentation will be compelling, and some of it will be accurate. At Amazon, the loop genuinely approaches something close. At Walmart, it is being built with intention and honesty about the gaps. At the other 80-plus US retail media networks competing for a market that is barely growing for anyone outside the top two, the closed loop is a marketing claim running on measurement infrastructure that a Fortune 500 consumer goods company, after years of systematic evaluation, found did not consistently deliver what was promised.

The corridor conversations at Possible 2026, between sessions and over dinner, are more instructive than the keynotes. Brand marketers who have run holdout experiments describe a gap between platform-reported ROAS and independently measured incrementality that, once seen, cannot be unseen. Media buyers who have managed campaigns across seven or eight networks simultaneously describe the operational overhead of managing seven or eight different attribution windows, seven or eight different data definitions, and seven or eight different dashboards, none of which speaks to any other, as something that makes budget allocation feel more like administrative management than strategic investment.

The measurement crisis is not a secret. Everyone in the industry knows it exists. The 6 percent trust figure is not a surprise to the people spending the $71 billion. It is a number they recognise. The crisis persists because the current system, whatever its limitations, produces ROAS numbers that are large enough to justify the next budget request, and because the retailers providing those numbers have structured their measurement methodology to ensure that outcome. The change will come not from a technical breakthrough but from brands refusing to accept measurement that the platform producing it also defines and certifies, and from AI agents routing around the sponsored product in ways that force the industry to build data infrastructure that makes products findable by machines and outcomes attributable to the advertising that preceded them.

John Wanamaker complained in 1876 that half of his advertising was wasted and he could not tell which half. Retail media raised $71 billion on the promise that it had finally answered his question. Six percent of the people spending that $71 billion believe the answer. The other 94 percent are still waiting, not for better technology, but for measurement that belongs to them rather than to the platform selling them the inventory.

Somewhere in a warehouse outside Dallas, $50 million worth of refrigerator door screens sits in the dark, counting nothing, measuring nothing, attributing nothing. The sensors that were supposed to close the loop were counting shadows. In retail media, they still are.

ABOUT THE AUTHOR

Amit Goel writes longform articles about digital media and advertising technology, careers, technology and product management at blog.careerplot.com. Previous articles in adtech domain covered demand-side adtech economics, programmatic supply chain margins, AI’s disruption of publisher economics, and the conflict between The Trade Desk and the agency holding companies. All financial data in this article is drawn from primary sources including company earnings releases and SEC filings. All quotes are attributed to named individuals and on record.