The Honest Broker - The Trade Desk, the Agency Cartel, and the $1 Billion Secret Nobody Was Supposed to Find

How a whistleblower lawsuit, an allegedly failed audit, and decade of debated fee pyramid blew up programmatic advertising's most important relationship leaving industry's self-proclaimed moral guard

Disclaimer: I am writing this to the best of my knowledge of whatever time I have spent in my professional life in the mediatech and adtech industry and whatever I could learn either from experience or from others or by media reports. In no way, it reflects on any insider information or anything that could be confidential. Also, it has no input from my current or any of the previous employers and is written in personal capacity with publicly available information. It is just my attempt to summarize the whole discourse that’s going on in recent times in the trade press about the adtech industry in general. This is my attempt to summarize everything as a knowledge base for people to learn more about adtech industry in general and how everyone has been operating for more than a decade. There are 100s of experts who know more than me and if you are one of them reading this, please comment or let me know about inaccuracies mentioned in any way. Like everyone else, Claude has helped me write this article in a journalistic tone to cover facts without adding my personal opinion. Lastly, if you are offended and are planning to sue me, please don’t. I am not so rich that you can make money of it.

Here is a story about a company that spent fifteen years building an industry on a simple, radical idea: tell the truth about what you charge, show buyers exactly what they are buying, and never work for both sides of a transaction at the same time. In an industry that had made opacity its art form and its business model, this was not just unusual. It was a genuine competitive threat — to everyone who had been making a comfortable living from the opacity.

Here is also a story about the very powerful companies that were built on the opposite principle — the idea that complexity, secrecy, and a creative relationship with client budgets could generate extraordinary income if advertisers never asked too many questions. These companies cheered The Trade Desk when it was useful to them. They championed it, partnered with it, named it their preferred technology. And then, when The Trade Desk’s growth began to illuminate exactly the practices they had been quietly running for years, some of them picked up a flag labelled ‘transparency’ and used it to beat the transparency company over the head.

This is a story with a genuine protagonist, a set of genuine conflicts of interest, and — in the spirit of honest journalism — one chapter where the protagonist also trips over its own shoelaces. In public. Loudly. More than once.

To understand all of it, you have to start not in 2026 but in 2009, in Ventura, California, where a man named Jeff Green decided to build something the advertising industry had never seen — and which certain parts of it were hoping it would never have to.

01

The Honest Broker — How Jeff Green Built the Company the Industry Needed

The programmatic advertising ecosystem that Jeff Green entered in 2009 was, to put it charitably, a confidence game with better branding. Advertisers handed enormous budgets to agencies. Agencies bought media on their behalf — or, increasingly, bought it for themselves at undisclosed prices and sold it to clients at a markup, keeping the difference. Supply-side platforms, ad exchanges, and demand-side platforms formed a chain of intermediaries each collecting a slice that was individually invisible but collectively vast. The entire system ran on a foundational assumption: that clients would not, or could not, look too closely.

Green and his co-founder Dave Pickles had both worked inside this system. They understood where the money went and why it went there. And they made a deliberate, calculated, and at the time quite contrarian bet: build a demand-side platform that was transparent about what it charged, worked exclusively for buyers and never for sellers, maintained no supply-side relationships that could create conflicts of interest, and showed advertisers precisely what they were buying, at what price, in what context.

This was not idealism. It was a business model built on a specific insight: the agencies whose clients were beginning to ask awkward questions about where all the money went would pay a premium to use a platform they could actually defend in a board meeting. The platform that made transparency its product would win in a market that was slowly, reluctantly, being forced to confront its own opacity.

“We saw that most of the DSPs had created channel conflicts for themselves. There was this chance to go to the agencies with the idea that we were going to power them, not compete with them.”

— Jeff Green, CEO, The Trade Desk — AdExchanger, 2016

The bet paid off beyond almost anyone’s expectations. The Trade Desk went public on September 21, 2016, priced at $18.00 per share. On that first day, it opened at $28.75 and closed at $30.10 — up 67% in a single session. Over the following years it delivered revenue growth above 25% annually with remarkable consistency. Customer retention stayed above 95% — a figure that speaks to something beyond contractual lock-in. It speaks to a platform that was, year after year, doing what it said it would do.

The company’s all-time high closing price was approximately $139–141, reached on December 4, 2024. At its market peak it was valued at tens of billions of dollars. And in 2021, in what was perhaps the most explicit public endorsement the company had ever received, Publicis Groupe — the world’s most valuable advertising holding company — announced that The Trade Desk would be the exclusive third-party DSP partner for Epsilon’s Core ID, Publicis’s flagship identity solution. The world’s biggest holdco naming TTD as its preferred technology partner. A formal declaration of trust in what Green had built.

File that one away carefully. We will need it in about six chapters.

The Trade Desk’s Structural Foundations — Why They Matter

Buy-side only: TTD has never operated a supply-side platform, never owned a media property, and never taken supply-side money. Its entire business model depends on advertisers getting good results — because that is the only reason they keep paying. No walled gardens: TTD does not own the inventory it trades and cannot secretly favour its own media. Transparent fees: TTD charges a disclosed technology fee on managed spend. No rebates, no principal mark-ups, no ‘non-product related income.’ These are structural facts about how the company is built, not marketing claims.

02

The Fire Alarm Nobody Wanted to Hear — 2016 and the Rebate Reckoning

In March 2015, a man named Jon Mandel stood up at the ANA Media Leadership Conference in Hollywood, Florida, and said the thing the entire room had been pretending was not true. Mandel, the former CEO of Mediacom, one of the world’s largest media agencies, alleged bluntly that media agencies were systematically collecting undisclosed rebates from media companies — payments for directing client budgets toward those media companies — and keeping the money rather than returning it to the clients whose spend had earned it.

The ANA commissioned a seven-month independent investigation by K2 Intelligence, one of the most reputable research firms in the field. The report landed in June 2016. One hundred and forty-three interviews. One hundred and fifty individual sources. The findings were unambiguous.

ANA / K2 Intelligence Report, June 2016 — Verified Public Document

Non-transparent practices including cash rebates were found to be ‘pervasive’ in the U.S. media ecosystem. Senior executives were aware of and had mandated some non-transparent practices. Markups on principal media transactions ranged from approximately 30% to 90%. Media buyers were ‘sometimes pressured or incentivised by their agency holding companies to direct client spend’ to principal media regardless of client best interests. Of 41 sources confirming rebate deals exist in the U.S., 34 confirmed the rebates were undisclosed to clients.

Five of the six major agency holding companies declined K2’s request to make current executives available for interview. The American Association of Advertising Agencies called the report ‘anonymous, inconclusive, and one-sided.’ The irony of an industry transparency report being called opaque by the companies who declined to participate in it was apparently lost on the people issuing the statement.

The industry moved on. Some contracts were updated. Some clients asked better questions for a while. The underlying practices did not disappear. They found new vocabulary — ‘principal-based buying,’ ‘inventory investment,’ ‘non-product related income’ — and in some cases simply grew. The Trade Desk kept building. Kept being transparent. Kept growing.

The 2016 ANA/K2 report is not ancient history. It is the context that makes the 2026 dispute comprehensible. Every executive at every agency holding company who is now raising transparency concerns about The Trade Desk was working in this industry when that report was published. Some of them had been interviewed for it.

03

The China Raid — When Allegation Became Criminal Investigation

In October 2023, Chinese law enforcement officers walked into GroupM’s offices in China. More than three employees were detained as part of a state investigation. The subject of the investigation was the systematic retention of client rebates — precisely the practice Jon Mandel had described at a conference in 2015, and precisely the practice documented in the ANA/K2 report in 2016. Seven years later, in one of the world’s largest advertising markets, employees of what was then the world’s largest media-buying network were being detained by police over it.

GroupM is the media-buying arm of WPP. Campaign Asia-Pacific had spent two years investigating rebate-driven practices in China linked to former GroupM employees. WPP confirmed the detentions publicly.

This Is Not an Allegation

A law enforcement raid is a documented legal event. Chinese authorities raided the offices of GroupM — WPP’s media-buying arm — and detained employees. The subject was the retention of client rebates. WPP confirmed the detentions. This is verified fact, not an accusation from a rival or a whistleblower.

The industry largely moved on. Some reporting, some concern, and then the news cycle continued. But the raid was a very loud data point: the practices documented as pervasive in the United States in 2016 were being treated as criminal violations in China in 2023. The same structural logic. A different jurisdiction’s patience.

04

OpenPath — When Transparency Becomes a Commercial Threat

In 2022, The Trade Desk launched OpenPath, its direct-to-publisher buying programme. The concept was both elegant and threatening to a large number of people who had been making money from the absence of what it offered. OpenPath allowed advertisers to buy publisher inventory directly, bypassing the chain of supply-side platforms and intermediaries that each took a cut before the money reached the publisher. More of the advertiser’s budget reaches actual content. A cleaner, more verifiable supply chain.

Jeff Green positioned it as exactly what it was: a transparency tool. Publishers liked it because they received more money. Advertisers liked it because they received better value. By 2025 it had more than 400 publisher partners integrated, and Green had publicly anticipated that year as the beginning of OpenPath’s ‘steep acceleration phase.’

The agencies did not like it, and the reason is not complicated. OpenPath performs, structurally, the function that agency trading desks sell to clients as a service. When a transparent DSP tool performs supply-path optimisation transparently, at cost, the agency’s ability to charge clients for that optimisation — and, more significantly, to execute those optimisations in ways that also happen to generate proprietary margin — becomes very hard to justify.

In late February 2026, AdWeek exclusively reported that Dentsu had quietly disabled OpenPath entirely, after using it since its 2022 launch. WPP had withdrawn shortly after the programme’s launch and had never used it in markets including Australia. Both agencies cited concerns about fee visibility and uncertainty about ad placement transparency.

The Trade Desk’s CMO Ian Colley responded directly and specifically on LinkedIn: ‘TTD doesn’t push spend to OpenPath. It’s not a marketplace or curated inventory. OpenPath is offered at cost to the ecosystem. We’ve been clear about that. There are no hidden fees beyond that. If OpenPath is selected by an advertiser, it is because it represents the cleanest and most cost-efficient path.’

Worth Noting on Both Sides

The agencies’ stated concerns about OpenPath fee transparency have not been independently verified by any published audit. However, the commercial incentive to raise those concerns — since OpenPath competes directly with services agencies charge for — exists entirely independently of whether the concerns are valid. Both things can be true simultaneously: TTD may have had imperfections in OpenPath’s communication, and the agencies may also have had financial motives for exiting that had nothing to do with their clients’ interests. The timing also matters: OpenPath launched in 2022. The agencies did not exit in 2022. They exited in late 2025 and early 2026, at a moment when TTD was at its most commercially vulnerable.

05

Richard Foster and the Report That Became a $100 Million Lawsuit

Richard Foster spent seventeen years at GroupM, WPP’s media-buying arm — now rebranded as WPP Media. He rose to become the Global CEO of Motion Content Group, GroupM’s entertainment investment division. His division co-produced more than 2,500 television series during his tenure, including Love Island, and managed roughly $500 million in annual GroupM entertainment investment. In his final year, his US operation reportedly posted 140% revenue growth. He established Motion Content Group in May 2017, specifically structured to operate independently from GroupM Trading’s media inventory practices, and focused on compliance with client contractual obligations. He was, by any measure, a successful and long-serving senior executive.

In December 2024, Brian Lesser — the incoming CEO of GroupM, which was in the process of being rebranded as WPP Media — asked Foster to prepare a strategic assessment of the division’s operations and potential. Foster produced what became known internally as Project Claridges: an approximately 35-36 page document that did two things simultaneously. It outlined a proposal for a new consolidated entertainment division projected to generate net sales exceeding $2 billion by 2029 at profit margins above 70%. And it raised serious internal concerns about GroupM’s trading practices, concerns Foster had first raised internally as far back as a 2016 meeting with former GroupM executives.

What the Lawsuit Alleges — With WPP’s Response

The following is what Foster’s lawsuit alleges. WPP has filed a motion to dismiss, disputes the material characterisation of all practices, and the case is before the courts with no ruling yet issued.

According to the complaint, GroupM used its approximately $60 billion in annual client advertising spend to negotiate volume-based discounts and rebates from media vendors. Rather than returning these benefits to clients, the complaint alleges GroupM reclassified the resulting inventory as ‘proprietary media,’ sold it back to clients through opt-in agreements, and booked the spread as what internal documents reportedly called ‘non-product related income.’ An internal presentation Foster submitted as part of the Project Claridges report allegedly estimated GroupM derived nearly $1 billion annually from this income stream, with an internal growth target of 15% per year. Foster estimated that over the period 2019 to 2024, GroupM generated $3 to $4 billion from such deals and improperly retained approximately $1.5 to $2 billion of it.

According to the complaint, when Foster submitted the report, Lesser initially expressed concern and said he would investigate. He then, unbeknownst to Foster, forwarded the original report to Mark Patterson — the executive responsible for GroupM’s trading activities. Patterson is currently WPP Media’s Global President of Markets and Business Operations. Hours after Lesser separately asked Foster via text to produce a ‘sanitised’ version of the report excluding criticism of GroupM, a restructure was announced placing Foster’s division under Patterson’s direct oversight. Foster alleges he was then excluded from key meetings, removed from deals he had built, and gradually isolated from decision-making. On July 10, 2025 — the day after WPP’s stock fell 18% on a trading update disclosing serious deterioration at WPP Media — Foster was fired.

In November 2025, Foster filed the lawsuit in the Supreme Court of New York, seeking more than $100 million in damages. He alleges wrongful termination, retaliation, and violations of whistleblower protection statutes in California and New York. The individual executives named as relevant non-parties in the complaint include Mark Patterson (WPP Media’s Global President of Markets and Business Operations), Andrew Meaden (Global Head of Investment at WPP Media), and Nicola McCormick (Global General Counsel for GroupM). The specific allegations against each are described in the complaint, which WPP disputes in full.

WPP’s Defence — In Full, as Published

WPP has filed a motion to dismiss. Its key arguments, as reported by Digiday based on court filings, are: (1) According to a sworn affirmation from Lesser, Foster’s counsel sent WPP a draft complaint on October 10, 2025 — more than two months before filing — and threatened to go public unless GroupM agreed to a large severance payment within 30 days. WPP argues offering to stay silent for a payout is incompatible with being a whistleblower. (2) WPP contends Project Claridges contains no mention of illegal activity and is a business proposal tied to Foster’s own ambitions, not a whistleblower document. (3) Foster was among hundreds of U.S. employees let go in a routine organisational restructuring. WPP states: ‘The court has not yet made any findings in relation to the allegations and we will defend them vigorously.’

The Number From WPP’s Own Filing

Among the internal documents that entered the public record through WPP’s own court filings was a piece of data that is striking on its face. Across GroupM’s top 30 U.S. clients — representing $13.4 billion in total billings — 97.4% of the proprietary inventory from which GroupM was allegedly generating income had not been used by the opted-in clients. Google, GroupM’s single largest U.S. client at $2.3 billion in annual billings, had utilised just 0.51% of the proprietary inventory its budget was helping to generate. This data was in WPP’s own filing, submitted as part of its motion to dismiss, and was first reported by The Times and subsequently by Digiday.

WPP’s purpose in submitting these documents was to characterise Project Claridges as a routine business proposal rather than a whistleblower disclosure. The commercial picture the documents created in the public record was not something WPP anticipated becoming the story. Ivan Fernandes, a former WPP executive now advising other groups, described the filing as ‘commercially significant’ in comments reported by The Times.

“97.4%. That is the share of GroupM’s proprietary inventory that its own largest clients were not using. Google — its biggest U.S. client at $2.3 billion a year — had used 0.51%.”

— Internal GroupM data submitted in WPP’s own court filing, Foster v. WPP, publicly reported by The Times and Digiday, February 2026

The case is ongoing. No court has made findings on any of the allegations. Both the specific claims and the defences deserve to be heard in full before conclusions are drawn. What is clear is that the financial picture described in the publicly filed documents has given the advertising industry’s clients a great deal to think about.

06

Agencies Take the High Ground — A Brief and Ironic History

It is worth documenting, clearly and chronologically, how enthusiastically the major agency holding companies supported The Trade Desk — before they found it commercially inconvenient to do so.

When TTD went public in 2016, holding company trading desks were among its most significant clients. GroupM, Publicis’s Starcom, IPG’s Mediabrands, Dentsu — all were buying through TTD, recommending it to clients, and in several cases publicly praising its approach. The model Green had built — powering the agencies rather than competing with them — was working exactly as intended. The agencies loved having a best-in-class transparent DSP they could point to when clients asked awkward questions about programmatic buying.

In 2021, Publicis named TTD the exclusive third-party DSP partner for its Epsilon Core ID. Not a quiet commercial arrangement. A loud, public endorsement from the world’s largest advertising holding company by market capitalisation, telling the market: we trust this platform above all others.

The dynamic began shifting after 2022, as The Trade Desk launched a series of initiatives that were simultaneously transparency tools and competitive threats to specific agency revenue lines. OpenPath (2022) competed with agency supply-path services. Kokai (2023-24) automated functions agencies traditionally charged for. OpenAds (2025) built an alternative auction infrastructure. Ventura (2025) put TTD into the CTV operating system business. Each was framed accurately as advancing the open internet. Each also happened to undermine a specific way agencies were extracting margin from client budgets.

The Progression — From Partner to Auditor: A Verified Timeline

2016-2021: Agencies enthusiastically use and recommend TTD. GroupM, Starcom, Mediabrands, Dentsu all buy through the platform.

2021: Publicis names TTD exclusive DSP partner for Epsilon Core ID — a flagship public endorsement.

2022: TTD launches OpenPath, directly competing with agency supply-path optimisation services.

2023-24: Kokai AI platform automates campaign functions agencies charge for. TTD and agencies begin to experience operational friction.

2025: WPP and Dentsu quietly exit OpenPath, citing fee and transparency concerns. TTD launches OpenAds and Ventura. WPP stock falls 62% in 2025. Foster lawsuit filed November 2025.

Early 2026: Publicis commissions FirmDecisions audit of TTD. Issues memo advising clients to stop using it. The relationship publicly celebrated in 2021 becomes, five years later, the subject of a client advisory.

“It bothers me when leaders of non-transparent business models are critical of those of us who are setting the bar — especially when they advocate for moving dollars to more opaque platforms and transaction methods.”

— Jeff Green, CEO, The Trade Desk — LinkedIn, March 2026

Green’s frustration is understandable and his characterisation is, on the available facts, substantially supported. The companies now auditing TTD’s fee structure are the same companies whose practices were documented in the 2016 K2 report, whose Chinese offices were raided in 2023, and whose internal documents — submitted in their own court filings — describe a financial model whose beneficiaries, according to those same documents, were not primarily the clients whose budgets funded it.

The question is not whether the agencies are hypocritical. The question is whether their specific concerns about TTD are valid. Those are different questions, and conflating them is a mistake both sides have made.

07

The Epsilon SSP — Transparency Concerns, Apply Elsewhere

In September 2025, AdWeek exclusively reported that over the prior 18 months, the media-buying arms of WPP, IPG, Dentsu, Havas, and at least four independent agencies had been purchasing ad inventory indirectly through Publicis’s own Epsilon supply-side platform. In some cases, apparently without full visibility into where their supply chain was routing client money.

Publicis, through its 2019 acquisition of Epsilon for $4.4 billion, had built an SSP that was operating as a competitor to other agency holding companies. The agencies buying through it were, at least in some cases, routing client budgets through a direct rival’s infrastructure, potentially giving that rival access to buying patterns, audience data, and campaign intelligence.

No one commissioned an independent audit of this situation. No holding company issued a client memo advising its clients to pause using the relevant supply chain until the conflict was reviewed. The trade press covered it, the industry discussed it, and life continued. The contrast with the formal audit process subsequently applied to The Trade Desk is a question worth sitting with.

08

The Trade Desk’s Difficult Year — In the Spirit of Honest Reporting

A story told fairly requires honesty about the protagonist’s stumbles alongside its strengths. The Trade Desk had a difficult 2025 that was not entirely other people’s fault, and deserves to be reported as such.

The First Earnings Miss in Company History

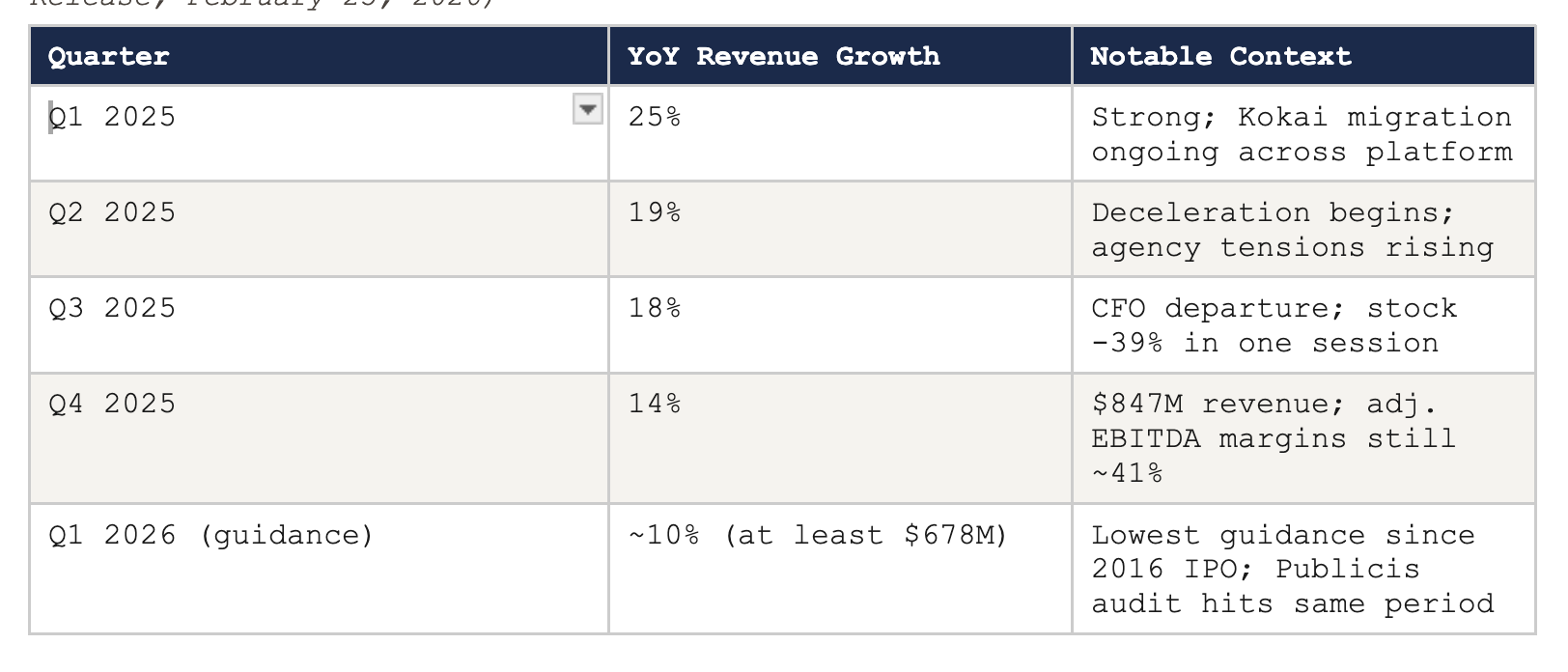

In the fourth quarter of 2024, The Trade Desk missed its quarterly earnings expectations for the first time in its history as a public company. Bank of America’s analysts cited one primary factor in their note: poor execution on the rollout of Kokai, TTD’s AI-powered campaign management platform. Agencies that had used TTD’s familiar interface for years were asked to adopt a new system, and TTD’s onboarding support was not adequate to the scale of the transition. Clients experienced frustration. Campaigns ran less efficiently during the migration. Revenue guidance came in below expectations. CEO Jeff Green issued a rare public apology to investors. The stock fell approximately 25% on the news.

Two CFOs in Under Twelve Months

In August 2025, TTD announced that CFO Laura Schenkein — a long-serving company veteran — was departing, to be replaced by Alex Kayyal, a board member from Lightspeed Ventures with no prior experience as a public-company CFO. The announcement was paired with a revenue miss and conservative guidance. The stock fell approximately 39% in a single trading session — the worst day in TTD’s history as a public company. Green issued a public apology to investors at the time.

Kayyal was then terminated effective January 24, 2026. He had been CFO for approximately five months. Tahnil Davis, the Chief Accounting Officer and an 11-year company veteran, was named interim CFO. Two CFOs in under twelve months at a company whose brand identity rests substantially on stability and trustworthiness is a self-inflicted wound. The agencies did not cause it. Good governance requires better.

Revenue Deceleration — Context Matters Both Ways

The Trade Desk — Revenue Growth Deceleration, 2025 (Source: TTD Q4 2025 Earnings Release, February 25, 2026)

The deceleration is real and material. Amazon Ads reported 23% year-on-year growth in Q4 2025 — compared to TTD’s 14% — and was reportedly offering DSP fees as low as 1% to major spending clients in direct competition. The broader programmatic market grew; TTD’s relative position weakened. These are real competitive dynamics, not simply the result of agency pressure.

Operational Friction

Digiday’s February 2026 reporting documented operational friction beyond the CFO situation. A media director at one mid-sized agency described cycling through three separate TTD account teams in under a year — three rounds of introductions, three attempts to rebuild working context on a platform complex enough that continuity is operationally critical. A separate executive described an incident where TTD threatened mid-contract rate increases when spending was pacing below an agreed annual target, then backed down when the agency threatened to move spend. Customer retention above 95% over eleven consecutive years means the vast majority of clients do not have these experiences. But the experiences are real, and a platform that claims the transparency high ground has less tolerance for this kind of inconsistency than one that never made that claim.

What TTD Gets Right Despite Everything

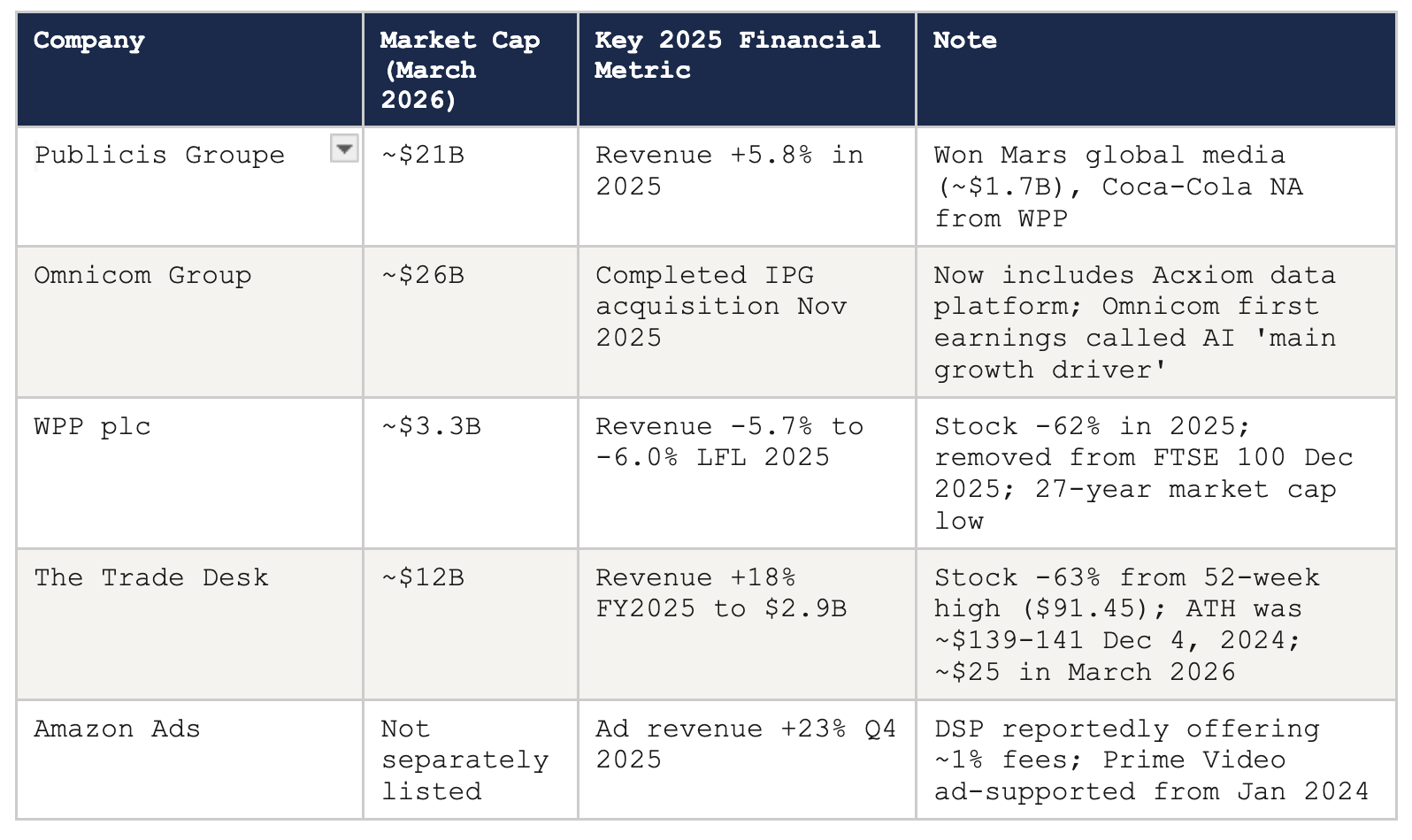

Full-year 2025 revenue was $2.9 billion, up 18% from 2024. Q4 2025 revenue was $847 million, up 14% year-on-year. Net income for 2025 was $443 million. Adjusted EBITDA margins were approximately 41%. The company carries no long-term debt and holds approximately $1.5 billion in cash. Customer retention has been above 95% for eleven consecutive years. Between March 2 and 4, 2026, Jeff Green personally purchased 6 million shares of TTD stock at weighted average prices between $23.49 and $25.08, totalling approximately $148 million — the largest insider stock purchase in the company’s history, per insider trading tracker Secform4, confirmed by an SEC Form 4 filing. These are the characteristics of a company with genuine structural strength navigating a difficult transition period.

09

The Allegedly Failed Audit — The Main Event

On March 17 and 18, 2026, Publicis Groupe — the company that had publicly named The Trade Desk its exclusive DSP partner just five years earlier — sent an email to select clients advising them it would no longer recommend TTD as a preferred DSP. The memo was based on an audit conducted by FirmDecisions, a unit of the Ebiquity Group. FirmDecisions is a credible, well-established media compliance auditor that had collaborated with the ANA on the K2 transparency report a decade earlier. Its institutional credibility is not in question.

The audit examined Publicis’s Master Services Agreement with TTD and, according to Publicis’s account of its findings, identified three specific concerns: that TTD had ‘improperly applied their DSP fee to other fees’ charged to Publicis and its clients; that Publicis and its clients had been billed for tools they were automatically opted into without authorisation; and that TTD had not provided the auditor with information necessary to validate that media and data costs were invoiced at cost without mark-up, as the agreement reportedly required.

Publicis stated it had engaged TTD’s senior leadership without reaching a satisfactory resolution. Stifel analyst Mark Kelley confirmed the same day that Publicis represents more than 10% of TTD’s gross billings — making it TTD’s largest holding company client. The stock fell approximately 5.7% on the news. Stifel characterised the move as likely a negotiating tactic, while downgrading the stock to reflect the financial risk.

The Word ‘Allegedly’ Is Doing Real Work Here

TTD ‘failing’ the audit is Publicis’s characterisation of FirmDecisions’ conclusions. The Trade Desk flatly disputes it. No court has ruled. No regulatory body has found a violation. What exists is a contractual dispute between a platform and its largest holding company client, mediated by an auditor whose findings one party accepts and the other specifically rejects. TTD states it has ‘never failed any audit ever’ in its history as a public company. This article uses ‘allegedly’ deliberately and accurately throughout.

The Trade Desk’s denial was specific and direct. In a company statement: ‘Any notion that TTD failed an audit is not true.’ The company argued that the auditor had requested data that would violate customer and partner confidentiality agreements — framing the refusal to provide certain information as a contractual necessity, not concealment.

Jeff Green took to LinkedIn with the broader argument about agency opacity. He is not wrong about the hypocrisy of agencies criticising TTD’s transparency while operating principal-based buying models, collecting rebates, and routing client spend through rival holding companies’ SSPs. He is also not, in addressing those arguments, specifically addressing the audit allegations. Those are two different things. Being more transparent than WPP is factually true, but it is not what resolving a FirmDecisions audit finding looks like.

The specific dispute — fee stacking, auto-opt-ins, refusal to validate cost claims — remains unresolved. TTD denies them. Publicis asserts them. FirmDecisions concluded them. No independent adjudicator has yet ruled. The word ‘failed’ is Publicis’s word, not a settled fact, and should be read as such.

10

Amazon, the Walled Gardens, and the Selective Transparency Standard

There is a third major actor in this story that rarely receives adequate scrutiny: Amazon Ads, which reported 23% year-on-year revenue growth in Q4 2025 while The Trade Desk reported 14%, and which was in 2025 reportedly offering DSP fees as low as 1% for major spending clients in a direct effort to attract agency budgets away from TTD.

Amazon’s structural advantages over any independent DSP are genuine and growing. It owns Prime Video, which launched ad-supported streaming in January 2024. It owns Thursday Night Football. It has the world’s largest e-commerce intent dataset. And it can trace an advertising impression to a purchase on Amazon.com in a way no independent DSP can replicate. At the 2025 Cannes Lions festival, Amazon Ads and Roku announced a partnership giving Amazon DSP exclusive authenticated access to logged-in Roku user data across more than 80 million U.S. households — the largest authenticated CTV footprint in the United States. In September 2025, Netflix announced advertisers could purchase Netflix inventory directly through Amazon DSP.

Green has argued, not entirely without basis, that Amazon’s ad business is approximately 90% Sponsored Listings competing with Google Search, not open-web programmatic display. Several agency buyers confirmed to Digiday in 2025 that Amazon DSP spend was ‘additive’ — from retail media budgets rather than trade desk budgets. This is plausible in the near term. Its durability as Amazon’s CTV ambitions mature is a different question.

The Transparency Standard Applied Selectively

The agencies auditing TTD’s fee structure route enormous budgets to Meta (ad revenue up approximately 21% in 2025), Google, and Amazon — platforms where advertiser transparency into auction mechanics, targeting logic, and fee structures is essentially zero. There are no FirmDecisions audits of Google’s ad exchange. There are no client memos about Meta’s auction opacity. There are no formal reviews of Amazon DSP fees when Amazon also owns the media. The Trade Desk — the one platform that publishes its fee structure and operates no owned media — is the one that received the formal audit. This observation does not resolve the audit findings against TTD. But it describes the environment in which they were commissioned.

11

WPP’s Freefall and the Industry’s Financial Pressures

Understanding why the agencies are fighting so hard right now requires understanding just how severe their financial situation has become. WPP’s story is the most dramatic illustration.

Agency Holding Companies vs. The Trade Desk — March 2026 (Sources: WPP 2025 Preliminary Results Feb 2026; StockAnalysis.com; PitchBook; TTD Q4 Earnings Release)

WPP’s market capitalisation of approximately $3.3 billion as of mid-March 2026 is smaller than the value of the accounts it lost to Publicis alone in 2025. The Mars global media account — approximately $1.7 billion — went to Publicis. The Coca-Cola North America media business — approximately $700 million — also went to Publicis. Its top 25 clients fell 4.1% like-for-like in 2025. WPP Media, its trading arm, declined 5.9% for the full year and 10.8% in Q4 alone. The company was removed from the FTSE 100 in December 2025. New CEO Cindy Rose acknowledged publicly that WPP Media had ‘lost its way.’

The structural pressure across all holdcos comes from the same source: AI is systematically compressing the cost of the functions agencies have historically been paid to perform — media planning, data analysis, creative iteration, audience segmentation. A 2025 Bannerflow report found 83% of senior brand marketers already use AI to target digital ads. Basis Technologies found 92% of advertising agencies use AI in some capacity. The margin that complexity used to justify is under pressure from every direction. WPP launched ‘WPP Open Pro’ in October 2025, a self-service AI marketing product for smaller clients — an acknowledgment in product form that its traditional service model cannot economically serve a large portion of its potential market.

In November 2025, Omnicom completed the acquisition of IPG — transforming the ‘Big Six’ holding companies into effectively a ‘Big Two or Three.’ The new Omnicom includes IPG’s Acxiom data platform, creating first-party data infrastructure competitive with platform data from Google and Meta. Publicis has Marcel AI and Epsilon. WPP has WPP Open. All of them are racing to demonstrate that their AI investments justify the fees they charge. The Trade Desk is watching from a position of financial strength but competitive vulnerability in this race.

12

The Clients Are Finally Noticing

The most striking statistic in the entire industry transparency conversation is from a 2025 World Federation of Advertisers report: 18% of marketers surveyed did not know whether principal-based buying had been part of their media activity in the past year. Not 18% who had concerns about it. 18% who did not know whether it had happened. This is the information asymmetry that makes the practices described in the Foster lawsuit possible at scale.

The ANA’s most recent benchmark found 54% of U.S. brands have an in-house media unit, and 51% have partially moved their programmatic buying function in-house. More than half of agency contracts, per the same WFA report, lacked clear penalties or enforcement mechanisms for principal-buying non-compliance.

Tucker Matheson, co-founder and managing partner of Markacy, told Digiday that his agency had moved spend toward direct buys and other platforms for a reason that is more honest than most: ‘TTD hadn’t done anything egregiously wrong — the alternatives had simply grown up.’ This is a useful corrective to narratives that frame every client departure as a verdict on TTD’s practices. Sometimes the market develops and dominant platforms face more competition. That is a legitimate commercial outcome, not a scandal.

The in-housing trend has genuine limits. Building a real in-house programmatic function requires technical expertise, organisational commitment, and ongoing investment that is not economically viable for most brands. The hybrid model — brand owns the DSP seat and the data relationship, agency manages execution — is the most common outcome. In this model, the agency’s margin on the technology layer disappears. The agency must compete on genuine intellectual value: strategy, creativity, analysis. This is, it turns out, what transparency looks like when it reaches the client relationship. It is not comfortable for business models built on the absence of it.

13

The Verdict — And What Comes Next

The Trade Desk built something that programmatic advertising genuinely needed. In an ecosystem structured around opacity, it built a platform on transparency. In a market where everyone was working both sides, it chose one side and stayed there for fifteen years. It delivered on that promise with sufficient consistency that 95% of its customers renewed, year after year.

The agencies that built their business models on the practices the K2 report documented in 2016 — the practices that led to law enforcement raids in China in 2023, to a $100 million whistleblower lawsuit in 2025, to internal documents describing a financial model whose primary beneficiaries, according to those documents, were not the clients paying for it — these agencies did not suddenly discover transparency concerns in 2026. They discovered that TTD’s growth was making their opacity structurally harder to maintain. And they reached for the language of transparency to address it, from a position whose relationship with that concept is, as the factual record demonstrates, complicated.

Jeff Green is right that the agencies auditing his platform are doing so from glass houses. He is right that an industry that routes vast budgets to Meta, Google, and Amazon without auditing their mechanics is applying transparency standards selectively. These are accurate observations.

Where TTD Must Do Better

The allegedly failed Publicis audit is not fully resolved by pointing at WPP’s court filings. TTD’s refusal to supply certain data to FirmDecisions — however contractually justified — is not what ‘passing an audit’ looks like to the clients observing the situation. The company that has spent fifteen years saying ‘look at how transparent we are’ cannot, at the first genuine audit stress-test of that claim, respond primarily by critiquing the auditor’s clients. The specific allegations — fee stacking, auto-opt-ins without authorisation, refusal to validate costs — deserve a specific, published, detailed response, not just a blanket denial.

Two CFOs in twelve months was a self-inflicted governance failure. The Kokai rollout execution was a genuine operational lapse for which Green publicly apologised. The account team instability reported by Digiday is correctable. These are real issues in a company that holds itself to a higher standard. Holding itself to that standard means addressing them.

The Structural Outlook

TTD’s financial position is stronger than its current narrative would suggest. Full-year 2025 revenue of $2.9 billion, up 18%. Net income $443 million. Adjusted EBITDA margins approximately 41%. $1.5 billion in cash. No long-term debt. Customer retention above 95% for eleven consecutive years. Jeff Green personally investing $148 million in his own company’s stock between March 2 and 4, 2026. These are not the characteristics of a company in existential crisis.

The agency holding companies face a harder structural question. The practices that generated margin in the past are under legal scrutiny through the Foster lawsuit, under client scrutiny through WFA transparency reporting, and under competitive scrutiny because the AI tools compressing their business are also making opacity harder to maintain at scale. Publicis and Omnicom, investing heavily in AI and data infrastructure, may navigate this transition. WPP, at $3.3 billion in market capitalisation with a CEO who has publicly acknowledged the company lost its way, faces an uphill climb.

The clients who fund the entire system have the most to gain from demanding genuine accountability from all sides. The 18% who do not know whether they participated in principal buying last year are subsidising a system that profits from their not knowing. That is an information problem, and the only people who can solve it are the ones writing the cheques.

“In an industry built on opacity, the most radical act is a straightforward fee schedule. The Trade Desk has been performing that act for fifteen years. The companies now auditing it have been performing a different one.”

— Analysis — AdTech Intelligence, March 2026

In programmatic advertising in 2026, everyone is standing in a glass house. The Trade Desk built its out of glass on purpose, because it understood that transparency is not just a principle — it is a competitive advantage, if you are actually committed to it. The question the next twelve months will answer is whether it remains committed to it under pressure. The question the industry needs to answer is whether it will hold all parties — not just the convenient one — to the same standard.

Somebody, at last, is watching. The question is who blinks first.

Read the second part of this article here :

Everybody Got Paid. Including the People Nobody Hired.

The Obligatory Disclaimer: I am writing this to the best of my knowledge of whatever time I have spent in my professional life in the mediatech and adtech industry and whatever I could learn either from experience or from others or by media reports. In no way, it reflects on any insider information or anything that could be confidential. Also, it has no…

SOURCES — VERIFIED PUBLIC RECORDS ONLY

All facts in this article are drawn from the following verified sources. Every claim traceable to a named, published document, court filing, or analyst note. All allegations from Foster v. WPP are attributed to the complaint. WPP disputes the material characterisation of all practices. No court has ruled. The case is ongoing.

ANA / K2 Intelligence — Media Transparency Initiative Full Report, June 2016 (public document)

AdWeek — Exclusive: Dentsu and WPP Quietly Exited The Trade Desk’s OpenPath, February 2026

AdWeek — Publicis advises clients to stop using The Trade Desk following allegedly failed audit, March 2026

AdWeek — Publicis-TTD Epsilon Core ID exclusive DSP partnership announcement, 2021

AdWeek — Publicis Epsilon SSP conflict-of-interest reporting, September 2025

Ian Colley, CMO, The Trade Desk — LinkedIn post on OpenPath allegations, February 2026 (verified verbatim)

Jeff Green, CEO, The Trade Desk — LinkedIn post on agency transparency, March 2026 (verified verbatim)

Jeff Green, CEO, The Trade Desk — AdExchanger interview on agency partnerships, 2016 (verified verbatim)

Jeff Green, CEO, The Trade Desk — Q4 2025 earnings call quote on competitive complexity, February 2026

Digiday — In Fighting a Whistleblower Suit, WPP Gave Away the Game, February/March 2026 (WPP motion to dismiss details, Project Claridges, executive descriptions)

Digiday — The Numbers Behind the WPP Whistleblower Case, March 2026 (97.4%, $13.4B, Google 0.51% stats)

Digiday — Agency Shopping Around on The Trade Desk, February 2026 (account team friction, rate increase incident)

Digiday — In-housing programmatic analysis, February 2026 (Tucker Matheson quote)

B&T Australia — Former WPP Exec Sues Holdco (detailed Foster complaint, executive roles), November 2025

Campaign Asia-Pacific — GroupM China rebate practices investigation and raid coverage, October 2023

Campaign US — Former CEO within WPP Media sues WPP (case filing details, verified roles), November 2025

Storyboard18 — Jeff Green LinkedIn post verbatim analysis, March 2026

Brewer Attorneys & Counselors — Official press release on Foster v. WPP filing, November 12, 2025

WPP plc — 2025 Preliminary Results and Strategy Update, February 2026 (revenue figures, account losses)

WPP plc — Q3 2025 Trading Update, October 2025

The Trade Desk — Q4 and Full Year 2025 Earnings Release, February 25, 2026 ($2.9B revenue, $847M Q4, net income $443M)

The Trade Desk — Q1 2026 Guidance ($678M minimum), February 2026

The Trade Desk — Ventura Ecosystem launch, February 24, 2026

The Trade Desk — OpenAds launch, October 2025 (first wave of publishing partners)

The Trade Desk — Official IPO press release, September 20, 2016 (priced at $18.00/share)

Nasdaq.com — TTD IPO first-day close $30.10, up 67%; September 21, 2016

MacroTrends — TTD all-time high closing price $139.51 on December 4, 2024; 52-week high $91.45

TradingView — TTD all-time high $141.53 on December 4, 2024; ATL $2.20 November 2016

SEC Form 4 filing — Jeff Green insider purchase, 6 million shares, $148M, March 2-4, 2026

Motley Fool — Jeff Green $148M purchase analysis, March 5, 2026 (confirms $23.49-$25.08 weighted avg)

Stifel Research — Analyst note: Publicis as >10% of TTD gross billings; likely negotiating tactic, March 2026

Bank of America — Analyst note citing Kokai execution as factor in Q4 2024 earnings miss

StockAnalysis.com — WPP market cap $3.28B as of March 18, 2026; TTD stock data

PitchBook / market data — Omnicom ~$26B market cap; Publicis ~$21B market cap, March 2026

ANA — In-house media benchmark report, 2023 (54% have in-house unit; 51% partially in-housed programmatic)

WFA (World Federation of Advertisers) — 2025 report: principal media, audit rights; 18% marketers unaware stat

W Media Research — Amazon and Roku CTV authenticated partnership, Cannes Lions 2025

Bannerflow / Basis Technologies — AI adoption statistics in advertising, 2025

The Times (UK) — Ivan Fernandes quote on WPP court filing commercial significance (reported in Digiday)

Court filing — Foster v. WPP plc and GroupM Worldwide LLC d/b/a WPP Media, filed November 2025 / December 2025, Supreme Court of New York, New York County / US District Court Southern District of New York

Amazing deep dive. Thorough.

This is a thorough piece and the agency hypocrisy argument is real and documented. But it misses the client perspective entirely, so here it is, from direct experience.

TTD charged fees without notifying us or getting approval from our media buyers. Not a billing dispute discovered in an audit. Real-time, active charges for tools we hadn’t authorized, added on top of contracted fees. When I raised this directly with their team, multiple calls, senior level but their response was unambiguous: this is how the platform works and we won’t change it. The effective fee rate ran 10-15% above what we had contracted.

We stopped working with them within weeks.

The agencies being non-transparent doesn’t make TTD transparent. What Publicis named in their audit, some of us experienced directly and decided not to wait for an audit to resolve it.