Everybody Got Paid. Including the People Nobody Hired.

A 2020 independent audit found 15% of programmatic spend attributed to nobody. The industry called it a reasonable business model and moved on. AI agents in 2026 are calling it a starting point.

The Obligatory Disclaimer: I am writing this to the best of my knowledge of whatever time I have spent in my professional life in the mediatech and adtech industry and whatever I could learn either from experience or from others or by media reports. In no way, it reflects on any insider information or anything that could be confidential. Also, it has no input from my current or any of the previous employers and is written in personal capacity with publicly available information. It is just my attempt to summarize the whole discourse that’s going on in recent times in the trade press about the adtech industry in general. This is my attempt to summarize everything as a knowledge base for people to learn more about adtech industry in general and how everyone has been operating for more than a decade. There are 100s of experts who know more than me and if you are one of them reading this, please comment or let me know about inaccuracies mentioned in any way. Like everyone else, Claude has helped me write this article in a journalistic tone to cover facts without adding my personal opinion. Lastly, if you are offended and are planning to sue me, please don’t. I am not so rich that you can make money of it.

Why This Article Exists

The first article ( The Honest Broker - The Trade Desk, the Agency Cartel, and the $1 Billion Secret Nobody Was Supposed to Find ) attracted considerably more attention than expected, and the conversations that followed were genuinely illuminating. Brand-side practitioners, agency people, publishers, platform executives, all of them said far more specific things in private messages than they were willing to say publicly. Dozens of DMs. A series of Zoom calls with people who wanted to go further. The pattern was consistent: strong, specific opinions shared in private that the same people would not put their name to in public. The clearest recurring theme: pointing at someone else’s opacity does not make your own opacity acceptable. Several people from the brand side described discovering platform fee overcharges through real-time campaign monitoring, not through a formal audit, and being told directly by the platform that this was simply how it worked. That sentence, delivered without apparent embarrassment, is the most concise description of this industry’s culture that anyone offered. And all of it — the DMs, the calls, the private frustrations that cannot be said in public — pushed me toward a question I had not asked clearly enough in the first article. Not “who is doing this?” but “why does the structure make it possible?” Which meant going back to first principles.

Around the same time, Vinny Rinaldi, VP Consumer Connections, at The Hershey Company, published a LinkedIn piece called ‘Stop Pointing. Start Building.’ His core point: everyone built this model, everyone profited from it, and now everyone is pointing at someone else. He is right. But the conversations I had after the first article suggested the problem was structural rather than merely behavioural, and that the solution ran through publisher technology as much as through advertiser contracts. And so I did something I probably should have done before writing the first article: I went back to first principles. I stopped thinking about adtech as a set of industry problems and started thinking about what adtech actually is, at its most basic level. What I found there is the frame for everything in this piece. This second piece is an attempt to explain the whole structure: who built it, who benefits from it, what AI and new technical standards are about to do to it, and why the people who want to understand where this goes next need to stop reaching for the industry vocabulary and start asking the simple questions first.

Nobody, and I genuinely mean nobody on the planet, woke up this morning hoping to see an advertisement. Not one person set their alarm earlier than necessary to catch a pre-roll video. No one booked bandwidth for a programmatic display unit. The person reading the New York Times did not pay thirty dollars a month for a digital subscription because they wanted to be followed around the internet for six weeks by a mattress brand.

Advertising is a tax. Specifically, it is a tax that consumers pay in the currency of attention and time, in exchange for content they actually want. That is the deal. It is a reasonable deal. Premium journalism, streaming entertainment, newsletters, podcasts, sports coverage, specialist blogs across 190 countries, users get all of this either free or below production cost because advertisers pick up part of the bill in exchange for showing their products to the people consuming that content. The user tolerates the ad. The publisher gets paid. The advertiser reaches an audience. Everybody goes home, if not exactly thrilled, then at least functional.

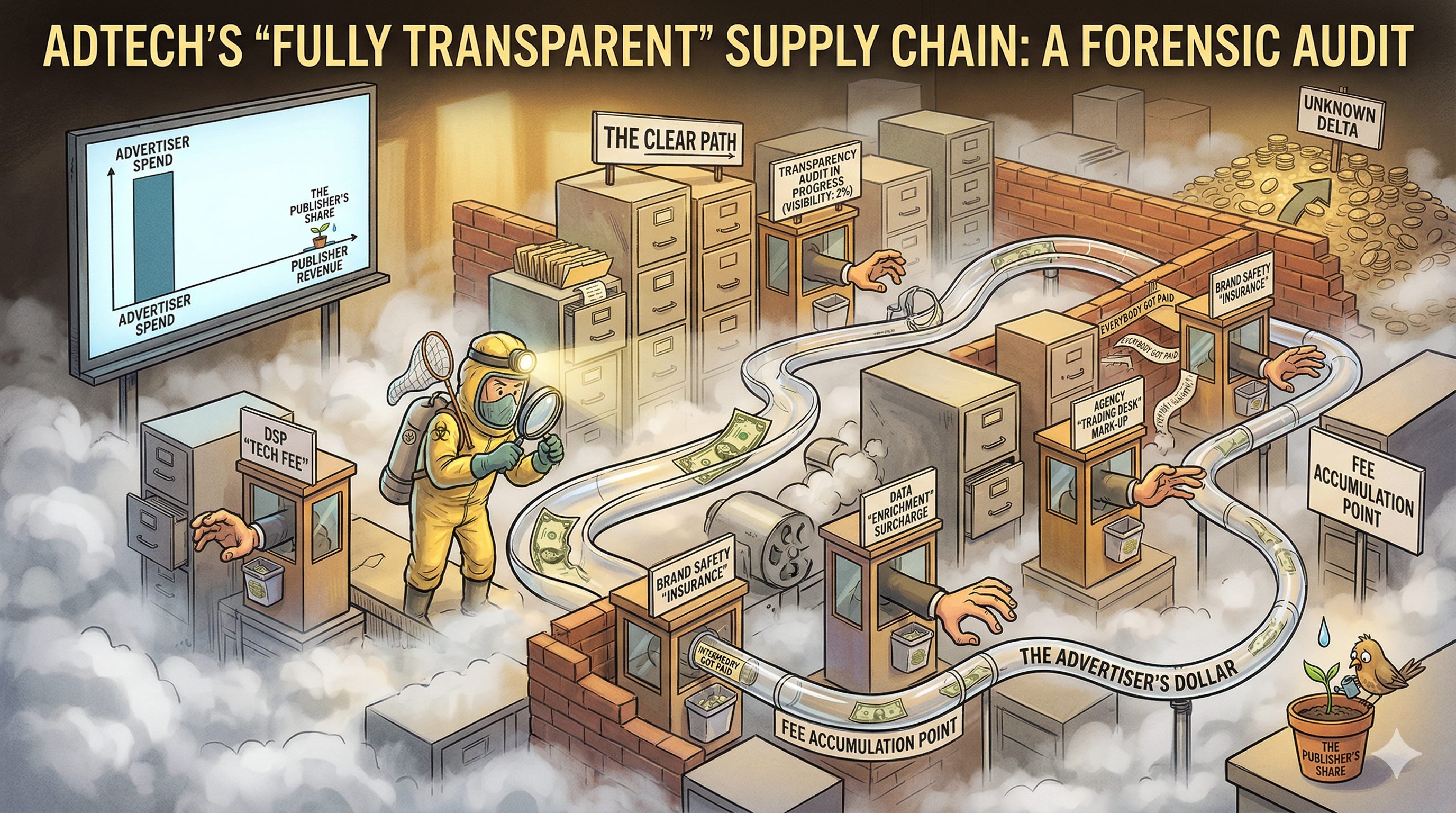

Before we go any further, stop. Stop and ask yourself a genuinely simple question: what is adtech, really? Not what the industry calls it. Not what the conference circuit describes it as. What is it, from first principles? Strip away the acronyms. Strip away the trade press vocabulary. Strip away fifteen years of white papers and working groups. What you are left with is this: supply and demand. Publishers have content and audiences. Advertisers want to reach those audiences. That is the whole thing. Everything that exists between those two parties is, in plain old-fashioned business language, a middleman. That is not an insult. Middlemen exist in every industry, every market, every supply chain in human history. They can add genuine value — aggregating supply, reducing friction, creating liquidity. The question has never been whether middlemen exist. The question is whether they earn their position in the chain, or simply occupy it. That question is what this article is about. And it is a question the adtech industry has been remarkably reluctant to answer from the ground up.

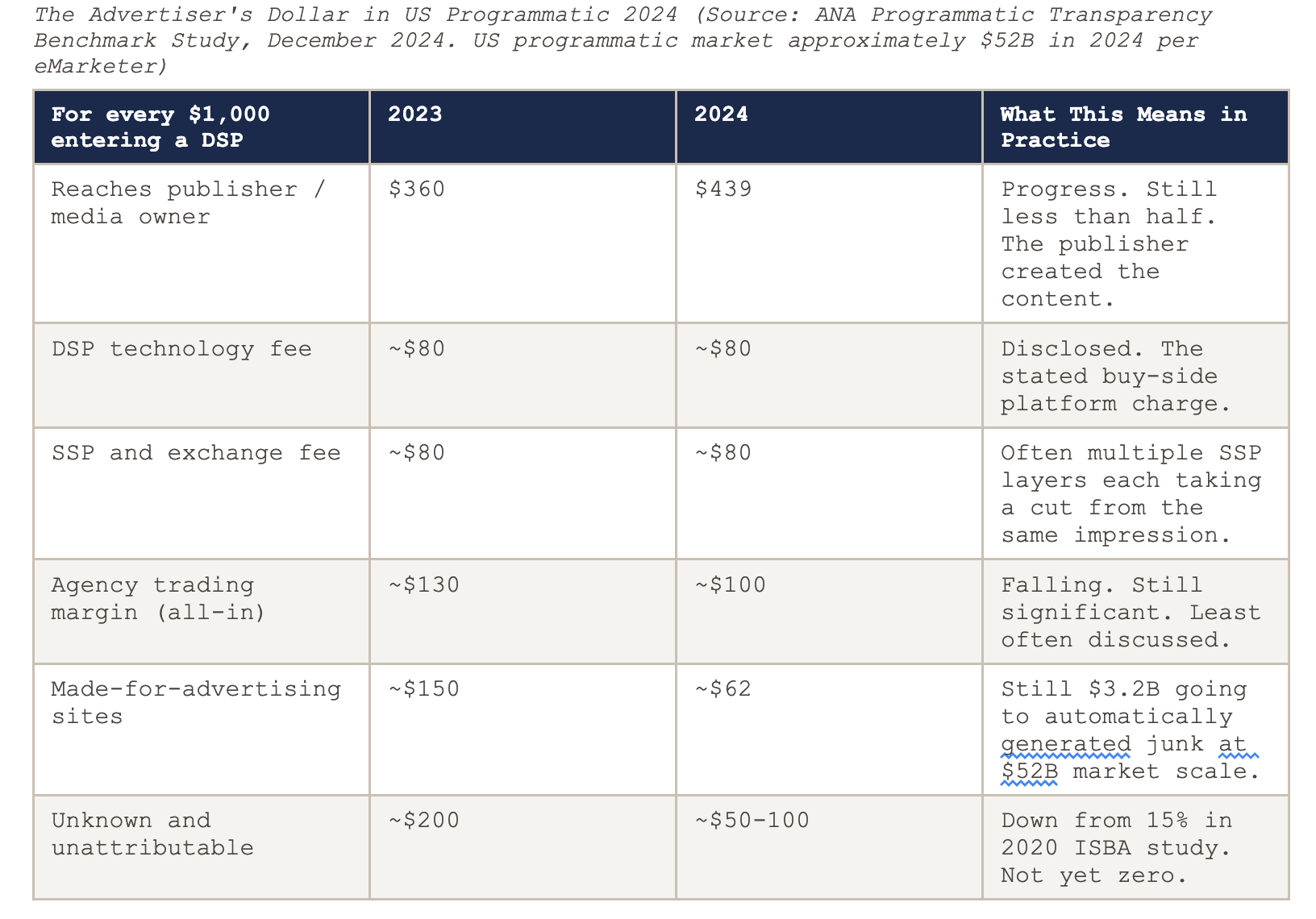

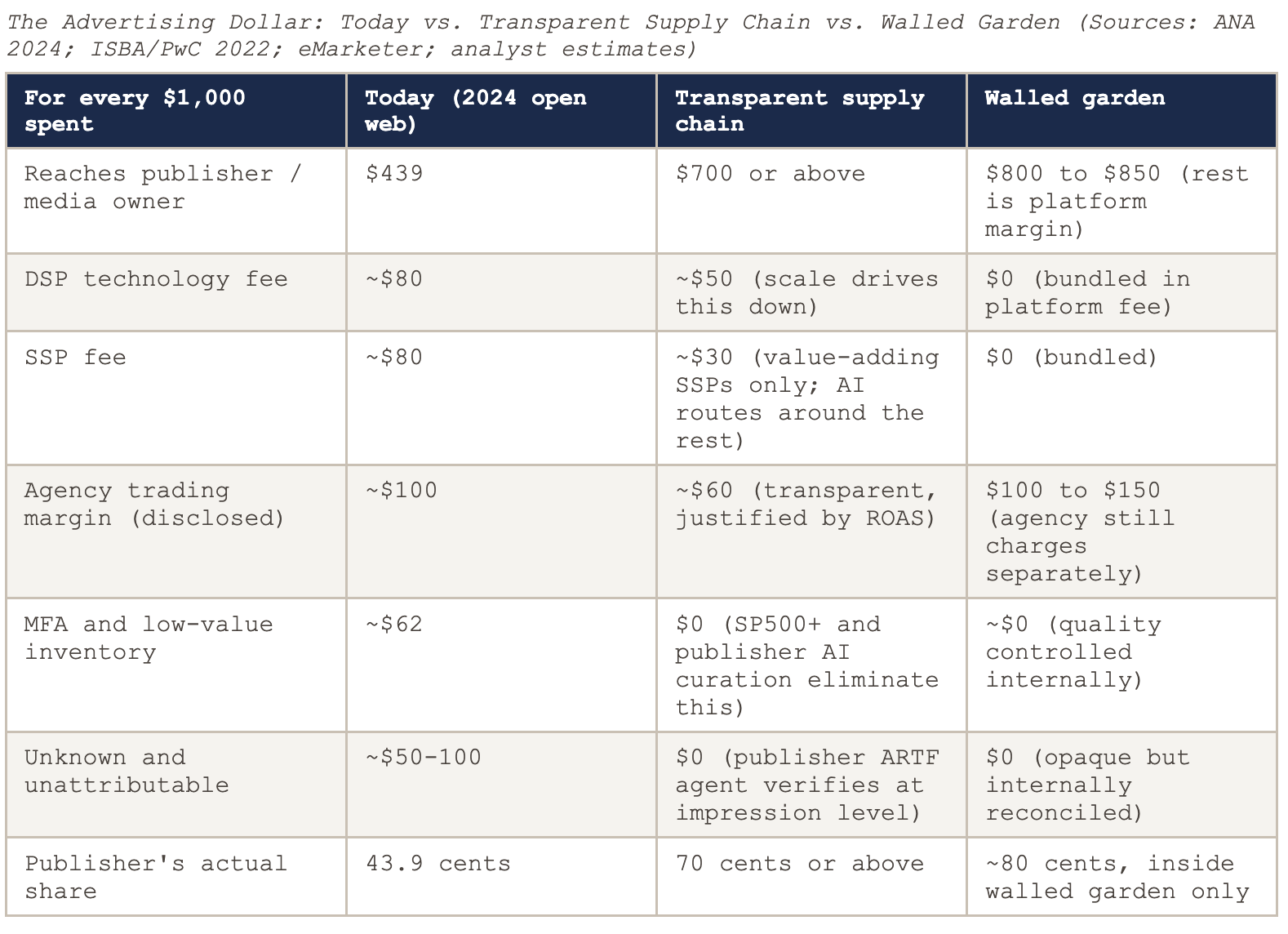

The problem is not the deal between the publisher and advertiser. The problem is the supply chain executing the deal. Between the advertiser who hands over the money and the publisher who is supposed to receive it, there are approximately forty different companies, each with their own technology stack, their own fee structure, their own auction mechanics, and their own sincere belief that their layer of this arrangement is entirely indispensable. By the time the money completes its journey, the publisher receives about forty-four cents of every dollar the advertiser spent. In 2020, the ISBA and PwC tracked one hundred million pounds in UK advertising spend and found fifteen percent of it attributed to nobody at all. Not to fraud. Not to a specific fee. Just to a gap in the universe.

The user is watching a show on Paramount Plus. The advertiser is spending a hundred thousand dollars to reach them. The publisher is receiving forty-four cents of that dollar. The other fifty-six cents are funding the most elaborate toll road in the history of commerce. Nobody commissioned the toll road. Everybody is using it. Everybody in it is getting paid. Including, as it turns out, the people nobody specifically hired to be there.

This article is about how that toll road was built, how AI is about to install cameras on every stretch of it, why publishers outside the walled gardens have more power than they are exercising, and why the open internet, the part that has been writing transparency pledges since 2016 while running practices that made transparency commercially inconvenient, is heading toward a reckoning it cannot write its way out of.

But first, we need to go to India at five in the morning. And then to a trading floor in New York in 2007. Both are relevant. Both are the same story.

01

The Farmer, the Bond Trader, and the Programmatic Supply Chain

A farmer in India loads his harvest onto a truck. Five months of work: seeds, fertilizer, water, labour, and the specific anxiety of someone whose entire year depends on the weather making two correct decisions in a row. He knows his production cost to the rupee. What he cannot know, because the market structure prevents him from knowing, is the price his grain will fetch at the regulated marketplace down the road. That information belongs to the licensed traders who operate there. They know the prices. They know each other. And they are not in the habit of sharing either.

Academic researchers studying agricultural supply chains in India found that for every one dollar a consumer pays more for food, the farmer receives two extra cents. Two. Out of a hundred. The Reserve Bank of India confirmed in its 2024 research bulletin that farmer income as a share of consumer price ranges from 28 percent to 78 percent depending on the crop. The farmers at the 28 percent end have learned to live with this mathematics. They do not have much choice. The information that determines the price sits with someone else.

Now, picture a trading floor in New York in 2007. American banks are issuing mortgages to people who will not be able to repay them. These mortgages are rated BBB. Then the banks package bundles of BBB mortgages together, hire ratings agencies to certify the resulting product as AAA, and sell it to pension funds as a safe instrument. The pension fund cannot see inside the package. The ratings agency certifying the quality is being paid by the bank that built the package.

“It’s a big pile of bonds bundled together. The genius part is that the banks thought they could package them together and spread the risk. But actually they were just piling up the risk.”

-- Ryan Gosling as Jared Vennett, The Big Short, 2015

Michael Lewis documented what happened next in his 2010 book The Big Short. Adam McKay made it into a film five years later. The key scene is a Jenga tower. Each block is a mortgage. Stack enough uncertain blocks the right way, apply the right label, and what was individually BBB becomes collectively AAA. The ratings agency says so. The pension fund buys it. The bank collects its fee.

Now, here is the programmatic advertising supply chain.

An agency trading desk buys digital advertising inventory in bulk. It buys some premium inventory: genuine quality publishers, real engaged audiences, brand-safe environments. It also buys made-for-advertising inventory, which is the polite industry term for automatically generated websites that exist solely to host ads, with traffic assembled to satisfy a targeting algorithm rather than to actually read anything. This mixed inventory gets packaged together as ‘proprietary media’ and sold to clients at a uniform premium price. The client cannot see inside the package any more than the pension fund could see inside the CDO. The entity certifying the quality of the bundle is the same entity selling it.

The ANA found in its 2024 benchmark that 6.2 percent of US programmatic spend, roughly $3.2 billion at $52 billion total market size, still landed on made-for-advertising sites, with some marketers directing more than 25 percent of their budgets there. The BBB inventory, dressed as AAA, sold at the AAA price. The publisher who created genuine premium content receives forty-four cents of the advertiser’s dollar. The farmer gets two cents.

The farmer in India, the 2007 pension fund manager, and the 2026 brand manager approving a programmatic budget are all living inside the same structural problem. Someone in the middle controls the information about what the product is actually worth and what price it traded at. The intermediaries are different in every story. The mechanism is identical in all three.

What Happens When Someone Actually Measures the Gap -- ISBA/PwC 2020 vs 2022

2020: ISBA and PwC tracked approximately 100 million pounds in UK ad spend across 15 major advertisers including Tesco, Unilever, and BT. Publishers received approximately 51 percent of advertiser spend. A further 15 percent (the ‘unknown delta’) could not be attributed to any known supply chain participant. Not to fraud. Not to a stated fee. To nobody. The Guardian received 30 pence per brand pound in its own controlled test.

2022 follow-up: publishers’ share rose to 65 percent. Unknown delta fell to 3 percent. The 14 percentage point improvement in publisher share came entirely from measurement and sustained industry pressure. Nobody improved their practices out of virtue. They improved because the data made their margin visible and clients started asking questions. That is the most important data point in the transparency debate: accountability works when it is quantified. Sources: ISBA/AOP/PwC Programmatic Supply Chain Transparency Studies, 2020 and 2022.

From 51 cents to 65 cents in two years, just from making the measurement public. No regulation. No litigation. No conference panel. Just data, published, visible to the clients paying for all of it. This is also, if you think about it, a fairly devastating commentary on what fifteen years of transparency white papers without measurement achieved.

02

Nobody Cares About Open Internet vs. Walled Gardens, Except the People Whose Margins Depend on You Caring

Here is a confession the advertising technology industry finds uncomfortable: advertisers do not have a religious preference for where their ads run. They are not emotionally attached to Google or philosophically committed to the open internet. They want to reach the people they need to reach, in contexts where those people are paying attention, at a price that produces a return. That is the entire brief. Full stop.

A chief marketing officer at a consumer goods company does not lie awake agonizing over whether their campaign runs on YouTube or the Washington Post or a podcast or a Substack newsletter. They lie awake wondering whether the campaign sold the product. The CMO who tells their board they achieved ‘strong reach and frequency metrics’ while declining to report revenue contribution is not long for their job in 2026, which is a recent development in the profession and a healthy one.

The walled gardens have been winning the budget argument not because advertisers love them but because they made ROAS measurement relatively easy to report, even if the methodology is controlled entirely by the platforms measuring themselves. Meta says your ad produced these conversions. Google says this search campaign drove this revenue. Amazon says these sponsored products generated these purchases. The open internet’s equivalent for many years was: trust us, it worked, here is a third-party viewability report and an audience segment that may or may not have seen the ad. One of these is a harder sell to a CFO who is now, for the first time, actively present in the marketing budget conversation.

The users are not in walled gardens because they love Meta’s advertising infrastructure. They are on Instagram because their friends are on Instagram. They are watching Prime Video because Amazon spent $8.5 billion acquiring MGM in 2022 and has been commissioning premium content ever since. They are on YouTube because YouTube has more video content than any human could watch in several lifetimes. The content and the community are there. The advertiser follows the user. The money follows the advertiser. The walled garden wins not because it invented better advertising technology but because it controls where attention goes, and then built an advertising business on top of that control.

Here is a first-principles point the open internet conversation consistently refuses to make clearly: walled gardens are not a violation of natural order. From basic business logic, they make complete sense. A walled garden owns the technology. It owns the user base. It provides services those users actively choose. It bears the cost of that relationship — the infrastructure, the content, the moderation, the product development. In exchange, it reserves the right to monetise that relationship as it sees fit. That is not opacity. That is a vertically integrated business doing exactly what vertically integrated businesses do. The term “open internet” was not coined because it was philosophically superior. It was coined because not everyone can be a walled garden. Can Paramount? In theory, yes. In practice, it requires billions in technology investment, a global user base of sufficient scale, and the organisational appetite to bear the full cost of building and operating all of it. The open internet exists because most publishers cannot clear that bar — not because the open model is inherently more virtuous. Once you understand that from first principles, the transparency argument changes shape entirely. The question is not why walled gardens are opaque. The question is why the open internet built a supply chain so complex that even its own participants could not account for where fifteen percent of the money went.

Also here is what the walled garden debate obscures: the audiences exist everywhere. The New York Times crossed 10 million digital subscribers in February 2023. Spotify has approximately 600 million monthly active users across 180 markets. Paramount Plus, Disney Plus, Warner Bros. Discovery’s streaming services, Bloomberg, the Financial Times, The Economist, and thousands of specialist publishers across 190 countries, these are not leftover audiences that advertisers have to settle for. In many categories they are better audiences than the walled garden alternatives: more engaged, more logged in, more willing to pay for what they are consuming, which tells you something specific and useful about their disposable income and the quality of their attention.

The advertiser who needs to reach financially active adults in their thirties and forties has a stronger argument for Bloomberg or the Financial Times than for Instagram Reels adjacent to a recipe video. The advertiser trying to reach sports fans in connected television has a better case for ESPN or a league-owned streaming service than for generic YouTube pre-rolls. Advertisers know this. The problem is that the open internet’s supply chain has been too busy collecting its own toll to demonstrate the value of the inventory it sits on top of.

The Statistical Sleight of Hand: Both Numbers Are Real and They Contradict Each Other

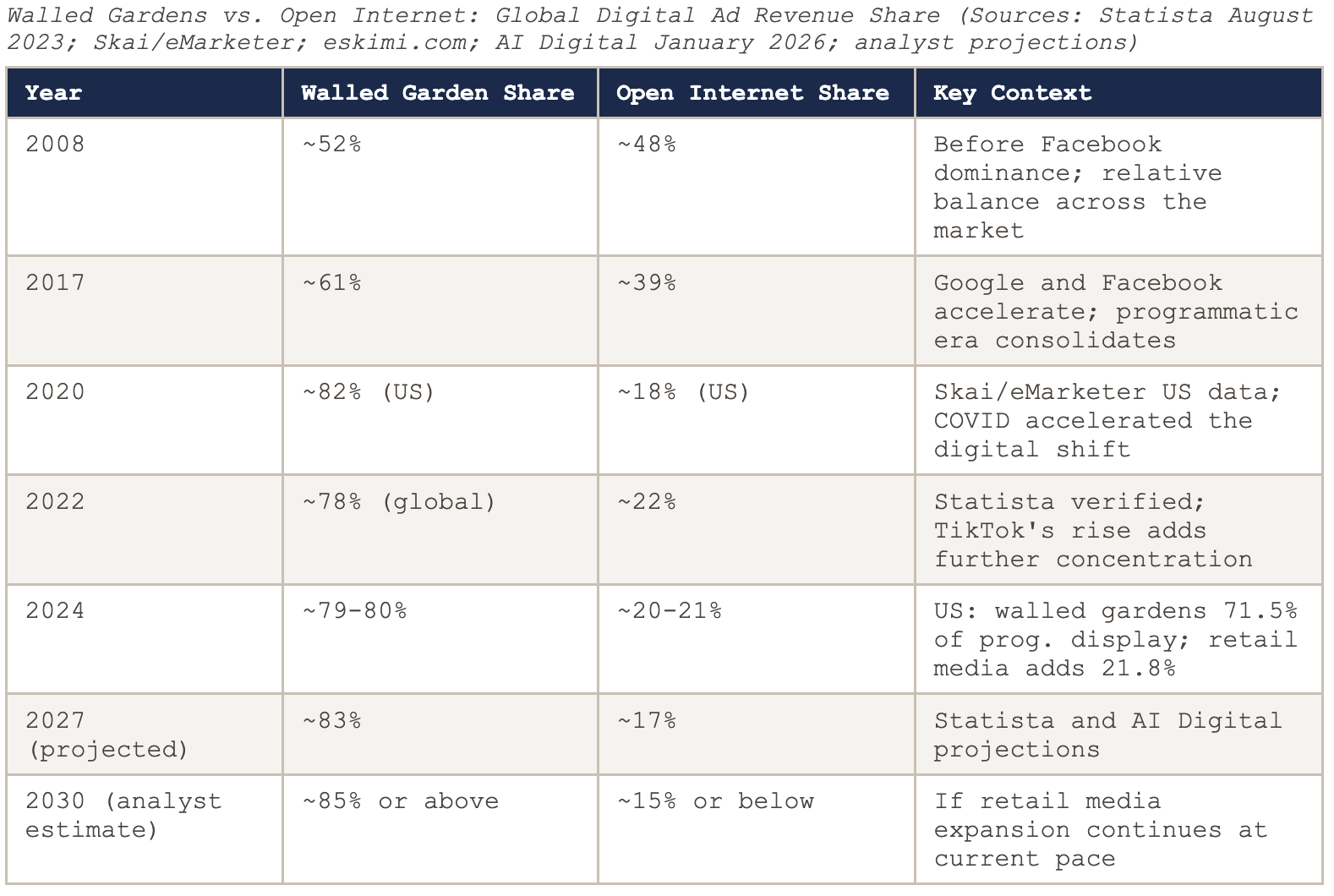

The open internet received more advertising money in absolute dollar terms in 2024 than in 2016. Total global digital ad spend grew to approximately $650 billion in 2024. In absolute terms, the open internet is a larger business than it was. In share terms, it went from approximately 48 percent of global digital advertising in 2008 to approximately 20 to 21 percent in 2024. New walled gardens are being created constantly: TikTok built one of the fastest-growing ad platforms in history from essentially zero after 2019 and now has approximately one billion monthly active users. Retailers, from Walmart to Target to Kroger to Tesco, have turned their customer data into closed advertising ecosystems. The market is expanding and the walled garden share of that expanding market is growing faster than the open internet’s share. In the long race, the open internet is losing ground every year even as the cheque it receives gets slightly larger. Focusing on absolute growth to avoid discussing relative decline is precisely the kind of statistical framing that has allowed the industry to avoid the harder conversation for a decade.

03

How the Supply Chain Got Built, and Why It Stayed Complicated

Take a step back further. Adtech as a distinct industry started because the internet happened. With the internet came cookies — a mechanism for remembering who had visited what, which advertisers and publishers latched onto as the infrastructure for targeting and tracking. The rest of the tech world moved on from third-party cookies relatively quickly. Adtech did not. The entire programmatic ecosystem was built on, and remained dependent on, cookie-based identity for roughly thirty years. When Google announced its Privacy Sandbox project to phase out third-party cookies in Chrome, the industry went into a sustained state of anxiety. When Google eventually abandoned the project in 2024, the collective sigh of relief across the industry was audible. Think about what that tells you from first principles: an industry that had three decades to develop a durable, privacy-respecting identity infrastructure had instead spent those three decades hoping nobody would take away the crutch. That is not a technology problem. That is a structural incentive problem. Real-time bidding, when it arrived, was a genuine innovation. But if you look at it honestly, RTB in practice has never been true bidding in the classical economic sense. True bidding produces price discovery — a clearing price that reflects what the inventory is genuinely worth to the buyer who values it most. What RTB produced in practice was closer to a waterfall with extra steps: a structured sequence in which certain buyers get preferential access, floor prices are set opaquely, and the “winning bid” often reflects who had the best positioning in the queue rather than who had the highest genuine valuation. Header bidding emerged specifically to address this — to give publishers a mechanism to run a more genuinely simultaneous auction across multiple demand sources. It was the market’s own correction for the structural distortion that RTB had introduced. All of this, cookies, RTB, header bidding, the proliferation of SSPs and DSPs, happened not because someone designed a rational architecture from first principles, but because each layer solved the immediate problem created by the previous layer, while generating the conditions for the next layer to extract its own margin.

Programmatic advertising’s origin was legitimate. In 2007, publishers had unsold remnant inventory and no efficient way to reach multiple buyers simultaneously. DoubleClick was acquired by Google in 2007 for $3.1 billion because it had built infrastructure the market genuinely needed. The supply-side platform, the ad exchange, and the demand-side platform were real solutions to real market problems. The companies building them created genuine value and were correctly rewarded for it.

Then the market did what markets do when the original problem is solved and the money is still flowing. New entrants arrived. By 2014 the IAB had counted more than 1,000 advertising technology companies operating across the stack. Supply-side platforms proliferated. Supply path optimisation, which became a significant industry practice from 2019 onward, was the market’s first honest acknowledgment that the supply chain had developed a redundancy problem. When buyers started asking which of these hundred intermediary paths was actually necessary, the ISBA/PwC answer was: we cannot tell you where 15 percent of your money went, and the publisher at the end of the chain is receiving 51 cents of your pound.

Here is the core of the issue, stated from first principles: the entire adtech supply chain grew the way it did because publishers did not know how to price their own inventory and advertisers did not know their return on investment in any quantitative, verifiable sense. That is it. That is the whole explanation. When the seller does not know the value of what they are selling and the buyer cannot measure what they are getting, the middle fills with people who are very confident about the value of their own contribution. Advertisers burnt money on the advice of agencies, routed through DSPs, exchanges, SSPs, ad servers, chains of intermediaries stacked on top of each other, each extracting a fee at a point in the chain where neither the publisher upstream nor the advertiser downstream had full visibility. The result was that more than fifty cents of every programmatic dollar got absorbed before it reached the person who had created the content in the first place. The transparency debate — the white papers, the industry coalitions, the conference panels — was a downstream symptom of this upstream failure of price discovery. The Trade Desk built its entire commercial identity around transparency as a differentiator, and it worked, because nobody else was willing to make the same bet. That tells you everything about how the rest of the industry had chosen to compete.

“It is the murky at best, fraudulent at worst, media supply chain.”

-- Marc Pritchard, Chief Brand Officer, Procter and Gamble, IAB Annual Leadership Meeting, January 2017

Pritchard said that representing approximately $10 billion in annual advertising spend. The industry agreed, published white papers, and largely continued as before. Three years later, ISBA/PwC found 15 percent unattributable. The muck, it turned out, was load-bearing.

At $52 billion in US programmatic spend in 2024, with $439 per thousand reaching publishers, approximately $22.8 billion reached content creators. The other $29.2 billion went to fees, margins, MFA inventory, and a residual unknown category. In December 2024, the AdExchanger Transparency Benchmark found that 61 percent of media buyers said they did not fully trust reported auction fairness. After fifteen years of programmatic advertising, the majority of the people buying it do not trust how it works. That is not a measurement problem. That is a supply chain that has never been required to be fully honest about itself.

“Advertisers deserve to know what they are paying for, and why they lost or won an auction.”

-- Bob Liodice, President and CEO, ANA, ANA Transparency Task Force Report, February 2025

04

The 78 Percent Problem: The Open Internet Is Losing the Long Race

In 2008, walled gardens held approximately 52 percent of US digital advertising revenue. By 2020, per Skai’s analysis of eMarketer data, they held over 82 percent in the United States. Globally, Statista reported that walled gardens reached 78 percent of digital advertising revenue in 2022. The projected share for 2027 is 83 percent. Analyst consensus places the 2030 figure above 85 percent if the retail media expansion continues at its current pace.

Alphabet, Meta, and Amazon generated approximately $422 billion in advertising revenue in 2024, roughly 65 percent of total global digital ad spend outside China. Advertisers in the United States spent approximately $2.50 with walled gardens for every $1 on the open web. And the model is replicating. Amazon, Walmart, Target, Kroger, Tesco, JD.com, and dozens of other retailers have built closed advertising ecosystems around their own customer purchase data. TikTok reached approximately one billion monthly active users and built one of the fastest-growing ad platforms in history from essentially zero after 2019. Every new platform that achieves scale defaults to the walled garden model because the walled garden model is profitable, relatively defensible, and relatively easy to operate.

The open internet did not lose to walled gardens because it ran out of audiences, publishers, or content. It lost because a significant portion of its own intermediaries spent fifteen years competing on margin extraction rather than on demonstrable value creation. Google, Meta, and Amazon are opaque about their auction mechanics, targeting logic, and attribution methodology. The open internet’s claimed advantage over this was transparency. In practice, its own supply chain generated ‘unknown deltas’ of 15 percent, bundled made-for-advertising inventory with premium inventory, collected non-product-related income from client spend without client knowledge, and fought the audit tools that would have demonstrated its value. An industry that cannot account for 15 percent of a client’s spend does not win the transparency argument by stating it. Advertisers made a rational choice.

In Europe, the EU Digital Markets Act designated Google and Meta as gatekeepers in September 2023, imposing data sharing and interoperability obligations that created the first serious legal framework for challenging walled garden dominance. Early implementation has not changed market share but established the regulatory infrastructure that could eventually do so. In China, Alibaba, Tencent, ByteDance, and Baidu operate a parallel walled garden ecosystem entirely closed to Western programmatic infrastructure. In Southeast Asia, Grab and Shopee are building super-app media environments. The open programmatic internet as practised in the United States and Western Europe barely exists in most of Asia Pacific.

05

Why 2025 and 2026 Are Different: Three Reasons the Old Playbook Stops Working

The transparency debate is not new. The ANA and K2 Intelligence documented agency principal-media markups of 30 to 90 percent in 2016. The ISBA/PwC unknown delta was mapped in 2020. What is different now is that three forces are operating simultaneously, each making opacity more expensive to maintain than it was the year before.

The CFO Has Entered the Building

Between 2020 and 2022, cheap money and pandemic-driven digital growth made return-on-advertising-spend conversations aspirational rather than mandatory. US interest rates then rose to their highest level since 2007. Marketing budgets became the most visible discretionary cost on the P&L. CFOs who had been passive observers started requiring ROAS data rather than impressions reports. The question ‘where did the money go’ became a CFO question, and the answers that satisfied media operations teams for a decade did not satisfy CFOs.

AI Is Making the Invisible Visible

When a bidding algorithm manages campaign optimisation in real time at a fraction of the cost of a human trading desk, the question of what the trading desk was charging for becomes impossible to avoid. A 2025 Bannerflow survey found 83 percent of senior brand marketers already use AI to target digital ads. Basis Technologies found 92 percent of advertising agencies use AI in some capacity. The ANA’s 2024 benchmark found that private marketplace spend, where algorithmic curation replaced manual supply chain navigation, rose to 59 percent of programmatic, up from 41 percent in 2023. The manual work that was billed at margin is being automated. The billing structures have not changed at the same speed. That gap is where the new friction lives.

AI is also changing attribution measurement in ways that systematically disfavour opacity. Machine learning attribution models can now produce ROAS estimates with a precision that turns ‘did this campaign work’ from a narrative argument into a numbers argument. Numbers arguments are harder to win when the numbers show 43.9 cents reaching publishers and 6.2 percent going to made-for-advertising sites.

The Courts Produced What the Industry Would Not Volunteer

The US Department of Justice antitrust case against Google’s advertising technology, which went to trial in 2024, placed supply chain economics into a public court record with the specificity and authority that fifteen years of industry conferences could not. The WPP whistleblower case, which became public through WPP’s own court filings in November 2025, placed approximately $1 billion annually in what WPP’s internal documents called ‘non-product related income’ into evidence, with internal data showing 97.4 percent of the relevant clients were not using the inventory that generated that income. Neither disclosure was volunteered. Both were extracted by legal process.

Three Converging Forces: Why the Old Playbook Has a Shelf Life

CFO pressure: marketing must justify itself in revenue terms, not impressions. AI displacement: the manual work of trading desks is being automated, making the cost-for-value question impossible to ignore. Legal exposure: the DOJ antitrust trial and the WPP whistleblower filing put specific supply chain economics into public court records for the first time. Running an opaque supply chain was always expensive for the advertisers paying for it. In 2026, it is also becoming expensive for the intermediaries running it, because the information that justified the opacity is no longer available only to them.

06

Publishers Have More Power Than They Think, But Only If They Control the Technology

Here is the argument the publishing industry needs to make to itself, out loud, in 2026. The content is yours. The audience is yours. The first-party data, the logged-in user behaviour, the reading patterns, the subscription history, the content consumption signals, all of it is yours. The only thing that is not yours, and the only thing that determines what any of it is worth to an advertiser, is the technology sitting between your inventory and the advertiser’s demand. That technology, for most publishers outside the very largest, was built by someone else to serve someone else’s interests.

Consider the specific assets in play. The New York Times crossed 10 million digital subscribers in February 2023. Bloomberg has roughly 400,000 paid subscribers who are among the most financially active people on the planet. Spotify has approximately 600 million monthly active users across 180 markets. The Economist, the Financial Times, Paramount Plus, Disney Plus, Warner Bros. Discovery’s streaming services and thousands of specialist publishers in dozens of languages, these are not substitute audiences for Meta’s social graph. In many advertising categories they are superior audiences: more engaged, more verifiably identified, more contextually appropriate, and more willing to pay for what they are consuming, which is a reliable signal about disposable income.

The publisher whose logged-in subscriber audience receives a $3 CPM when that audience is worth $15 to the right advertiser does not have an audience problem. It has a supply chain problem. The supply chain between the publisher’s content and the advertiser’s budget has been too focused on its own margin to communicate the audience’s value clearly. The farmer’s wheat is better than the bulk trader claims. The bulk trader has never let the buyer see it without his label on it.

The SP500+: The Trade Desk Does What Nobody Else Would

In February 2024, The Trade Desk began beta testing a product called the Sellers and Publishers 500+, deliberately named to evoke the S&P 500. The concept: a curated, actively maintained list of premium open internet inventory sources, evaluated at the individual ad placement level rather than just the publisher level. Initial participants in the beta included the New York Times, Disney Plus, Hulu, ABC, and the Wall Street Journal. Spotify was added subsequently. The product is globally available across connected television, web, and digital audio.

The Trade Desk’s Marketplace Quality team, which does the thankless ongoing work of keeping made-for-advertising inventory and fraudulent traffic out of the platform, underpins the whole exercise. The SP500+ is essentially that quality work made visible and actionable for buyers: instead of maintaining their own exclusion lists, advertisers can select SP500+ inventory and outsource the quality management to The Trade Desk’s ongoing curation.

“We want to be the alternative to the walled gardens. The open internet needs a champion, and we intend to be that champion.”

-- Jeff Green, CEO, The Trade Desk, AdExchanger Industry Preview, January 2024

The SP500+ directly addresses the BBB-dressed-as-AAA problem. It creates a transparent, auditable definition of what ‘premium open internet’ actually means and makes it actionable with a single product choice. This is something an SSP, the IAB, a publishers’ trade body, or an industry consortium could have built years ago. None of them did, because defining quality means excluding inventory that someone is currently monetising, and nobody wanted to be the one who drew that line.

The legitimate concern the industry has expressed about this is worth stating plainly: if buyers route spend primarily through SP500+ inventory that The Trade Desk curates and controls the criteria for, the DSP has moved from being a neutral buy-side technology to being a gatekeeper of the open internet. Green’s structural argument, that TTD’s buy-side-only model prevents this from becoming a true walled garden because the company has no supply-side inventory to favour, is credible but not complete. The SP500+ is a significant expansion of what a DSP has historically been willing to decide unilaterally. You can acknowledge that the work was necessary and nobody else was doing it while also noting that it transfers considerable power to the entity curating the list.

The Ad Server: Where All the Truth Lives

The ad server is the technology that determines which ad appears on a publisher’s page, at what price, in what order, following what rules. It is the point in the supply chain where information asymmetry is smallest: the publisher knows what they received and, with direct access, the buyer knows what they paid. In display advertising, Google Ad Manager dominates publisher ad serving to a degree that forms a central argument in the DOJ antitrust case. The company selling publishers the technology that manages their inventory also operates the exchange that buys that inventory and the demand-side platform that bids on it. This is not a coincidence. It is a competitive strategy that the DOJ is currently examining in considerable detail.

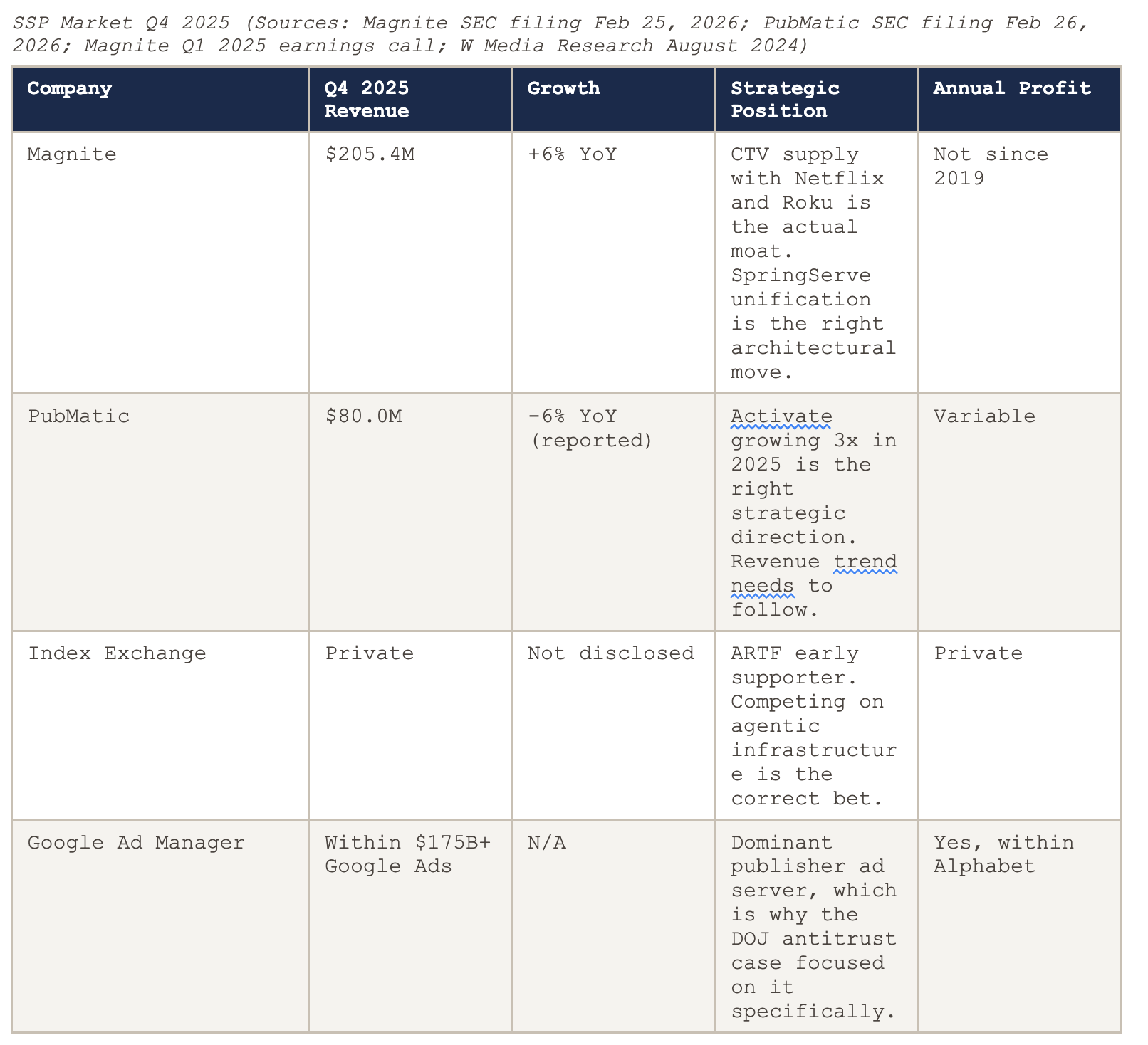

In connected television, two significant alternatives have emerged. Freewheel, acquired by Comcast in 2014, is the primary ad server for broadcast and cable networks making the transition to streaming. SpringServe, acquired by Magnite in 2021, became the principal independent alternative in the streaming space. And in April 2025, Magnite did something the industry had been debating for years: it actually merged the two.

On April 23, 2025, Magnite combined the SpringServe ad server with the programmatic capabilities of the Magnite Streaming SSP into a single unified CTV and OTT platform, initially in closed beta. Initial clients: Disney Advertising, LG Ad Solutions, Paramount, Roku, Samsung, and Warner Bros. Discovery. Jounce Media’s March 2025 Supply Path Benchmarking Report verified the platform connects buyers to 99 percent of US streaming supply on a dollar-weighted basis. General availability was targeted for early to mid-summer 2025. Sean Buckley, Magnite’s President of Revenue: ‘By unifying the programmatic layer as a complementary step in the buying process, it gives buyers greater transparency, predictability, and control over their ad placements, and lays the foundation for more effective monetisation and yield management for media owners.’

A publisher using Magnite’s unified SpringServe platform controls their yield management, their demand access, their supply path decisions, and their deal management in one system. That is a publisher operating as a technology company rather than as a technology customer. Will Doherty, SVP Inventory Development at The Trade Desk, endorsed the move directly at launch: ‘Magnite helps fuel the premium, open internet. Combined with tools like OpenPath, the next generation of SpringServe is accretive to advertisers and publishers.’ Two sides of the same transaction, for once, pointing in the same direction.

The unified ad server and SSP model is the correct architectural direction. A publisher who controls both the technology managing their inventory and the platform connecting it to demand has closed the information gap that has defined their relationship with the supply chain since programmatic began. They know what their wheat is worth. They can see what it traded for. They can compare the two. That is the foundation on which everything else in this article is built.

07

Agentic AI: The Technology That Enforces What Contracts Cannot

On November 13, 2025, the IAB Tech Lab released the Agentic RTB Framework, version 1.0, for public comment. If you missed the announcement in a busy November news cycle, here is what you missed: the most consequential technical standard in programmatic advertising since OpenRTB standardized the auction protocol in 2010.

The ARTF uses containerized architecture to bring demand-side platforms, supply-side platforms, data vendors, and bidding algorithms into the same virtual processing environment, reducing bid request-response latency by up to 80 percent, from the current 600 to 800 milliseconds to approximately 100 milliseconds. Netflix, Paramount, The Trade Desk, Yahoo, Index Exchange, and Chalice were among the early supporters. Anthony Katsur, CEO of IAB Tech Lab: ‘ARTF establishes a true control plane for an agentic future, where autonomous agents and specialised software enhance the bidstream in real time with rigour, safety, and interoperability.’ Joshua Prismon of Index Exchange called it ‘production-tested’ and ‘transformational’ at the November launch.

What the ARTF actually does, in plain language, is allow AI agents to operate inside the auction process as active verifiers rather than passive rule-followers. Within the microseconds available before a bid is placed, an AI agent can check whether the supply path for this specific impression matches the contracted route, whether the floor price the SSP declared matches what the publisher actually set, whether the inventory type is classified correctly, and whether the fee being applied is what was agreed in the contract. The 80 percent latency reduction is not an engineering efficiency. It is the time budget that makes real-time contract enforcement commercially feasible for the first time.

What ARTF Enables and What It Does Not Do Automatically

What it enables: per-impression supply path verification; real-time floor price confirmation; automated fee discrepancy detection across millions of transactions per hour; MFA and inventory quality evaluation within the auction window; and impression-level transaction records creating an auditable supply chain trail. What it does NOT do automatically: enforce anything. The technology detects discrepancies. It acts on them only if the contract specifies what action to take. An AI agent can halt spend on a non-compliant supply path automatically, but only if the buying contract says it should. The technology is the enabler. The contract is the instrument. The buyer or publisher who writes the rules the agent follows decides what actually changes.

Start on the Publisher Side, Not the Demand Side

There is a strong argument, and it is the correct argument, that AI agents should be introduced on the publisher side before the demand side deploys its own. Here is the logic. A demand-side AI agent built by or for an agency that profits from principal buying will be optimized for outcomes that preserve that profit. An SSP’s AI agent will be optimized for the SSP’s revenue. The only participant whose AI agent has no structural conflict of interest is the publisher. The publisher’s agent, sitting at the ad server, has one job: maximize the value of this impression for this publisher. It has nothing to gain from hiding the price from itself.

A publisher who deploys an ARTF-compatible AI agent at their ad server can verify, at the impression level, whether the floor price declared to buyers matches what the publisher actually set. Whether the winning demand source paid what it said it would. Whether the supply path routing matches the contract. The publisher’s agent is not trying to extract margin from anyone. It is trying to verify that the publisher received what it was owed.

When the publisher publishes those verified transaction records at the campaign and supply path level, they become the independent audit the industry has never produced voluntarily. A buyer’s AI agent can compare the publisher’s transaction record to its own. Discrepancies surface automatically. Contracts that specify consequences for discrepancies become enforceable in real time rather than through a formal audit process that takes weeks and produces a report that gets disputed for months.

The ARTF is not a finished product. Version 1.0 is a foundation. Adoption is in closed beta with initial supporters. But the IAB Tech Lab’s track record with OpenRTB, which became the universal auction standard within three years of its introduction, suggests that adoption will accelerate significantly in 2026 and 2027. The agencies and intermediaries that believe the business model they have run for twenty years will survive this shift are making the same bet that Blockbuster made when Netflix started mailing DVDs. The technology exists. The standard exists. The question is how quickly the contracts require it.

And this is where the first-principles argument becomes urgent rather than merely instructive. With agentic AI entering the adtech stack — with the IAB Tech Lab’s ARTF and the emerging AdCP standards creating the infrastructure for autonomous agents to operate inside the auction process — the industry is at a fork in the road. One path: deploy AI as a smarter version of the existing architecture, automating the same intermediary layers, preserving the same structural information asymmetries, making the same toll road faster and harder to audit. The other path: use AI to actually go back to basics. Supply and demand. Publisher and advertiser. A clear answer to the question “what is this inventory worth, and did the money reach the person who created it?” If the industry does not choose the second path consciously and deliberately, agentic AI will default to optimizing the first one, because that is the architecture it will inherit. The fundamentals do not disappear because the technology becomes more sophisticated. They become more consequential. An industry that cannot explain its own supply chain from first principles to a first-year economics student has no business layering autonomous agents on top of it and calling that progress. Stop. Think from the basics. Then build.

The Publisher-Led Agentic Supply Chain: How It Works in Practice

Step 1: Publisher controls its own ad server. In CTV, that now means Magnite’s unified SpringServe or Freewheel. In display and every other channel, it means an independent alternative to Google Ad Manager.

Step 2: Publisher activates first-party audience data within the ad server to demonstrate audience quality to buyers at the impression level.

Step 3: Publisher deploys an ARTF-compatible AI agent that verifies every transaction against contracted terms in real time and maintains an impression-level transaction record.

Step 4: Publisher negotiates contracts with SSPs and DSPs specifying that floor prices are verifiable in the transaction record, supply path routing is disclosed, and discrepancies trigger automatic consequences rather than letters to lawyers.

Step 5: The publisher’s verified transaction records are accessible to buying partners, creating the real-time audit trail that quarterly formal audits have never consistently produced. Every component of this stack exists today.

08

SSPs: The Data Platform or the Toll Booth

The supply-side platform was built to aggregate demand for publishers who could not independently access multiple buyers simultaneously. In 2015, that function justified twenty-plus independent SSPs. In 2026, direct connectivity tools like the PubMatic’s Activate platform, which grew more than threefold in 2025 and allows advertisers to buy directly within the SSP bypassing DSP intermediation, are all testing the same question: how many SSP layers does the supply chain actually need?

AI supply path optimization is the automated version of the question buyers have been asking manually since 2019. An AI agent routing spend to the best-performing supply paths, verified at the impression level, does not favour an intermediary that cannot demonstrate its contribution. The SSPs that have a future are the ones controlling something that AI cannot route around.

The One Asset Worth Building: Aggregated Publisher First-Party Data

Individual publishers have rich first-party audience data. Logged-in users. Behavioural signals within the publisher’s ecosystem. Content consumption patterns. The problem is that individual publishers outside the very largest cannot make this commercially valuable at scale on their own. A regional news publisher with two million monthly readers has excellent audience data. It cannot sell that data to global advertisers the way Meta can.

An SSP that aggregates first-party data across hundreds of publisher partners, with consent frameworks and publisher agreements that make the arrangement transparent, creates something no DSP can replicate through direct publisher connections: a scaled, consented, cross-publisher audience graph that is genuinely differentiated from walled garden data. The SSP that moves a publisher CPM from $3 to $5 by demonstrating, through aggregated audience data, that an impression reaches a logged-in user whose behaviour matches an advertiser’s target, is adding transparent, measurable, auditable value. The SSP that adds a margin to transactions it did not improve is the one that AI routes around.

Magnite has not posted an annual net profit since 2019 and invests over $200 million annually in R&D. On the Q1 2025 earnings call, CEO Michael Barrett’s primary growth argument was that the Google antitrust ruling ‘could significantly increase our monetization opportunities and market share, possibly as soon as next year.’ That may be true. It is also a strategy whose timeline is entirely outside Magnite’s control. The SpringServe unification is a more durable bet because it is entirely within Magnite’s control and delivers something publishers demonstrably want: a single system for their entire monetization operation. Building on that is the right path forward.

09

DSPs and Agencies: The Clock Is Running on Both

The demand-side platform is structurally the correct model for transparent programmatic buying. Works exclusively for the buyer. Charges a disclosed technology fee. Has no supply-side inventory to secretly favour. This is the commission agent from the grain market: declaring its fee openly, competing on service quality, passing the rest through. The model is right. The metric DSPs have historically competed on is wrong.

Reach, frequency, and cost per thousand impressions are activity metrics. Return on advertising spend is the outcome metric that actually matters. The DSP that consistently delivers better ROAS than its competitors can charge a higher technology fee and justify it with a verifiable track record. The DSP competing on CPM against Amazon, which reportedly offers fees as low as 1 percent for major spending clients because its real margin is on Prime Video and Thursday Night Football, is not going to win that argument on price alone.

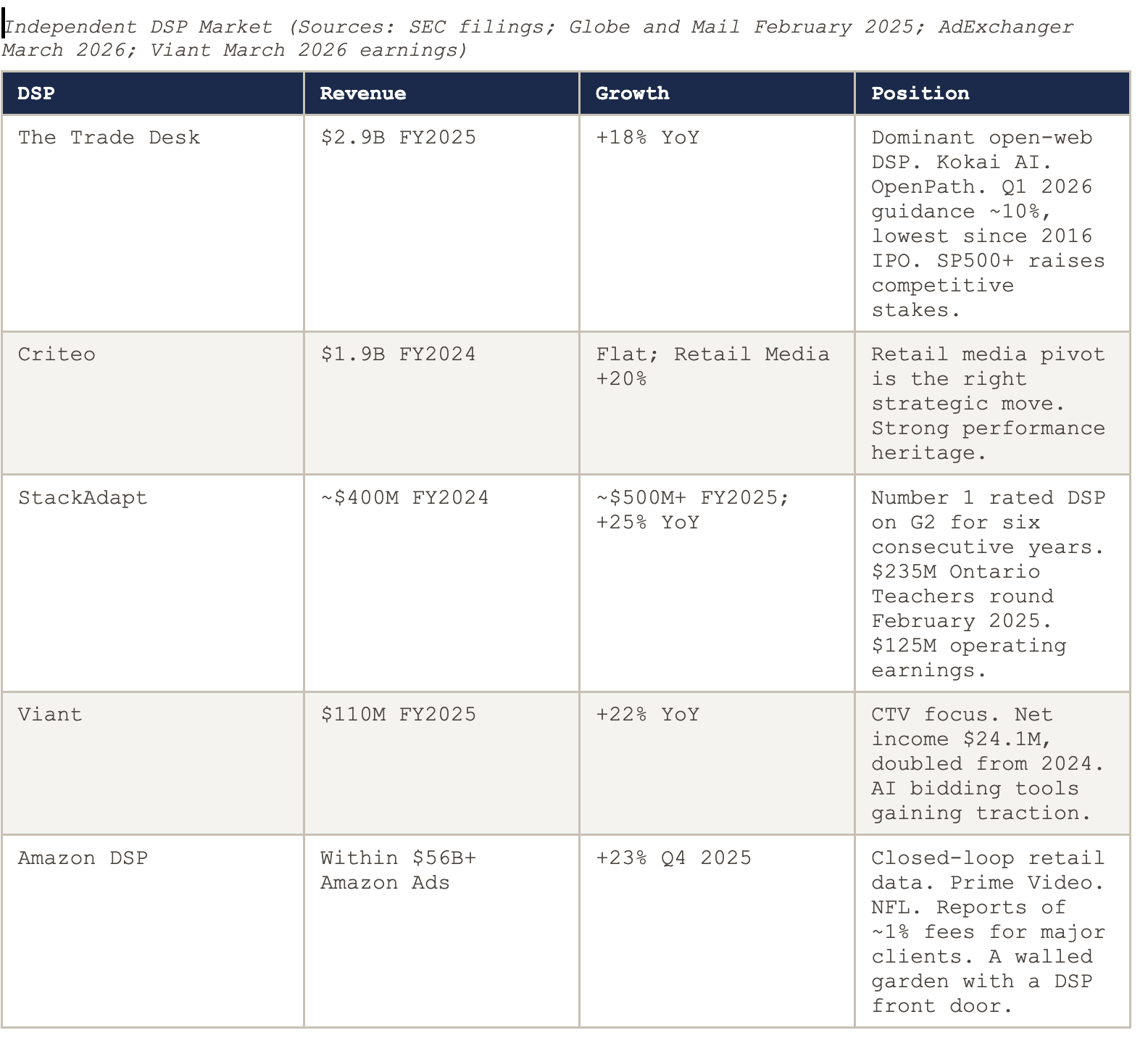

StackAdapt’s numbers are worth examining carefully. The Globe and Mail reported in February 2025 that StackAdapt generated nearly $400 million in revenue in FY2024 and was expected to surpass $500 million in FY2025 with more than $125 million in operating earnings, making it one of Canada’s most profitable private technology companies. Ontario Teachers’ Pension Plan led a $235 million funding round. Six consecutive years rated number one DSP on G2 by user satisfaction. Founded by former WPP employees who built the platform they wished existed when they were agency practitioners. That origin story tends to produce user-focused product development rather than billing-optimised product development, and the customer satisfaction ratings reflect it.

For agencies, the financial advisor parallel remains the clearest template. The UK Financial Conduct Authority’s Retail Distribution Review, effective January 2013, banned commission payments on retail investment advice and required advisors to charge explicit fees. The number of independent financial advisors fell from approximately 35,000 in 2011 to approximately 22,000 by 2014. The ones who left were the ones whose income depended on the commission structure rather than the quality of the advice. The ones who survived competed on demonstrable investment outcomes. WPP lost approximately 62 percent of its market value in 2025, saw WPP Media decline 10.8 percent in Q4 on a like-for-like basis, and lost the Mars global media account (approximately $1.7 billion) and the Coca-Cola North America media account (approximately $700 million) to Publicis. The financial advisor parallel does not require a regulator. The market is applying the same pressure on its own schedule.

10

The Supply Chain That Could Exist: A Dollar Comparison

The walled garden delivers 80 cents to the publisher because the publisher IS the walled garden. There is no external supply chain extracting a toll because the platform owns both sides of the transaction. The open internet’s answer to this cannot be another transparency pledge. It has to be 70 cents, delivered verifiably, confirmed by AI agents at the impression level, with ROAS outcomes that an independent firm can audit and compare to walled garden alternatives.

From 51 cents in 2020 to 65 cents in 2022 in the ISBA/PwC premium UK market study. From 36 cents in 2023 to 43.9 cents in 2024 in the broader ANA US benchmark. The trajectory is real. What accelerates it is publishers who control their own technology, advertisers who require log-level verification, SSPs that compete on publisher first-party data rather than inventory control, DSPs that publish ROAS benchmarks rather than reach metrics, agencies that separate advisory fees from execution margin, and AI agents whose rules are written by the people whose money is being spent.

11

The End: Or the End of the Beginning

Back to India for a moment. India’s e-NAM platform, the National Agriculture Market, launched in 2016 to give farmers access to the price information that licensed marketplace traders had held exclusively for decades. A farmer can now compare prices across multiple buyers, sell into distant markets, and verify that the weight recorded at the point of sale matches what was actually loaded. The system is imperfect. Implementation is uneven. Some traders have maintained advantages through side arrangements. But the structural condition that allowed two cents to the farmer and ninety-eight to the intermediary is being disrupted, slowly and unevenly, by the simple act of making price data publicly available.

The advertising technology industry’s e-NAM moment is arriving on multiple fronts simultaneously. The ARTF enables impression-level verification. The Magnite SpringServe unification gives CTV publishers integrated control over their ad serving and SSP in one system. The Trade Desk’s SP500+ creates the first actionable definition of premium open internet inventory. The DOJ antitrust case is extracting from Google the specific economic details of how publisher ad serving dominance translates into programmatic market power. AI attribution tools are making the revenue contribution of advertising spend measurable with a precision that did not exist three years ago. And the CFO is now in the room.

None of this requires virtue. None of it requires anyone to voluntarily give up income. The ISBA/PwC improvement from 51 cents to 65 cents reaching publishers came from measurement pressure, not moral awakening. The SP500+ exists because The Trade Desk calculated that cleaning up the open internet serves its own commercial interests. The Magnite SpringServe unification happened because publishers asked for it. Everything that is working is working because someone calculated that transparency was in their commercial interest. That is fine. That is how markets are supposed to work.

The open internet currently holds approximately 20 percent of global digital advertising. It is heading toward 17 percent by 2027 on current trajectory. Seventeen percent of an expanding market is still a large absolute number. But it is also a market that is losing competitive ground every year to platforms that are less diverse, less editorially independent, and less capable of reaching audiences across the full breadth of human content consumption. That matters for reasons beyond advertising economics. The publisher whose revenue falls cannot maintain the newsroom or the production budget or the creator community that made the audience worth advertising to in the first place.

The user watching a show on Paramount Plus, reading the Washington Post, listening to a podcast, scrolling a newsletter, all of them are tolerating the advertising because the advertising subsidizes the content they actually want. That is the deal. It is still a reasonable deal. It just requires the supply chain executing it to actually deliver the money to the people making the content, rather than treating the journey between advertiser and publisher as an opportunity for forty companies to clip the ticket.

The publishers sitting on those audiences have more leverage than they are currently exercising. The technology to exercise it exists today. The contracts to enforce it can be written this quarter. The AI agents to verify it in real time will be commercially widespread within two years. The only barrier is the institutional inertia of participants who benefit from the current arrangement and would prefer to keep discussing it at conferences rather than changing it at the contract level.

The farmers have smartphones now. The price data is available. The supply chain that built a business model on the farmer not having that information is going to have to find a different reason to exist.

Some of them will. The ones who add genuine value, who help publishers activate their audience data, who verify supply path integrity, who deliver ROAS outcomes that hold up under independent scrutiny, those intermediaries will thrive in the transparent supply chain because transparency confirms their value rather than threatening it.

The ones who got paid because nobody looked closely enough will find the next few years considerably more interesting than the last fifteen.

One last thing, and this is the reason this article exists. Every time adtech faces a genuine structural reckoning — privacy sandbox, the DOJ case, the ISBA/PwC findings, the arrival of AI — the industry’s first instinct is to reach for the vocabulary of the existing architecture. New technical standard? Build a working group. New privacy requirement? Launch a coalition. New technology? Retrofit it onto the current stack and give it a new acronym. That instinct is understandable. It is also the instinct that has kept the farmer at two cents and the pension fund manager holding AAA-rated BBB paper. The only way out is to stop, get off the bandwagon for a moment, and ask the genuinely simple questions. What is this industry, at its most basic level? Supply and demand. Publishers and advertisers. Anything in the middle needs to justify its existence by making that exchange more efficient and more valuable — not by making it more opaque. If your business model requires the publisher not to know what their inventory is worth, and the advertiser not to know where their money went, you are not adding value. You are making hay while the sun shines. And the sun, as this article has attempted to document in considerable empirical detail, is beginning to set on that particular field.

Everybody got paid. Including the people nobody hired. That part is about to get a lot harder to pull off.